Wire Fraud

Essential Elements, Examples, & How to Prevent

Partly because it has such a broad definition, wire fraud is one of the most commonly committed types of fraud today - with telemarketers, scam emails, and more constituting wire fraud.

As with anything, the best way to combat wire fraud is to truly understand what it is and how it works. We explore both, and then teach you how to prevent wire fraud from occurring on your platform. Let’s get to it.

What is Wire Fraud?

Wire fraud is any type of fraud conducted using interstate electronic communications to advance a fraudulent scheme. This includes communication via phone, email, fax, text message, social media, and other electronic messaging services.

Wire fraud is closely related to (and often confused with) mail fraud. While both are similar, there is one main difference. Mail fraud involves the use of the mail and postal services, while wire fraud simply involves electronic communication across interstate borders.

The reason that wire fraud is limited to interstate communications comes down to the jurisdiction of the regulatory body responsible for each type of fraud. While both are federal crimes that are charged by the Department of Justice, different regulatory bodies - with different jurisdictional responsibilities - enforce these laws.

Any use of the mail system in the US is regulated by the Postal Clause, which means all mail communications fall under their purview. However, since Congress derives its authority from the Commerce Clause, prosecution requires an interstate wire transmission for electronic communication to qualify as wire fraud.

What Constitutes Wire Fraud: Essential Elements

According to Section 1343 of the United States Department of Justice Criminal Manual, there are three essential elements of wire fraud:

- The fraudster devised or participated in a scheme intended to defraud another person or persons by means of false pretenses

- The fraudster knowingly and voluntarily participated in a scheme that was intended to defraud another person or persons

- The fraudster used interstate (or international) wire communications to further their fraud scheme

Ultimately, for an act to constitute wire fraud, the fraudster needs to have a willful intent to commit (or participate) in a fraud scheme, they must mislead the victim through false pretenses, and they must use wire communications to commit the fraud scheme.

How Does Wire Fraud Work?

Unlike other, more specific types of fraud, wire fraud is a broad, wide-reaching term. With such a broad definition, many different types of behavior - and even other types of fraud - fall under the scope of wire fraud.

Whether the fraudster steals money, valuables, or personal information, as long as they’ve used electronic communications to persuade their victims, they’ve committed wire fraud.

The participating party doesn’t need to be successful in their attempts to defraud someone to be convicted; they simply need to attempt to defraud someone. They don’t even need to have sent the deceptive communications themselves; if they had knowledge of or were involved in the scheme to mislead the victim, they can be held liable for wire fraud.

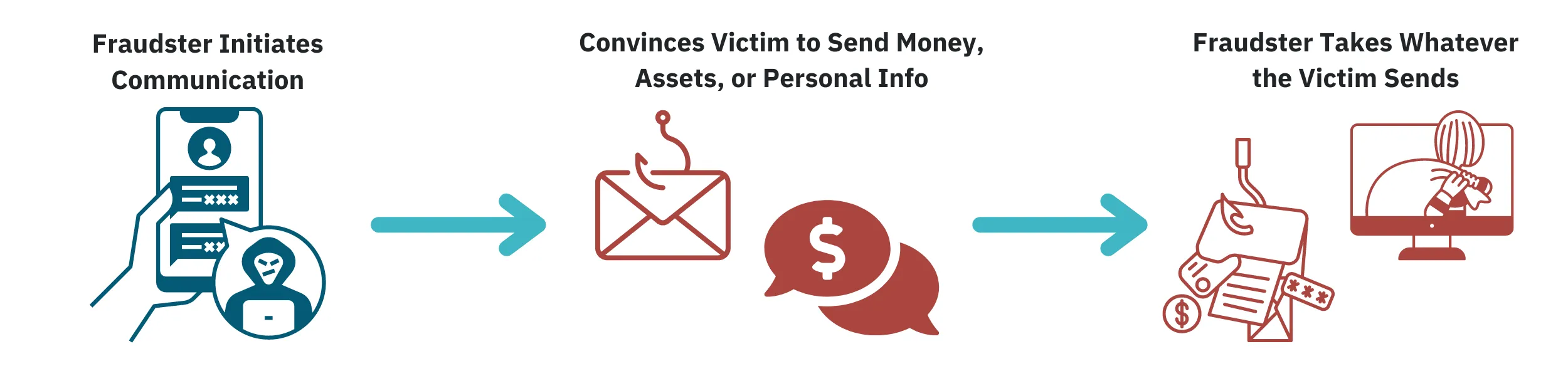

Below, we explain exactly how wire fraud works:

- The fraudster initiates contact via wired communication.

- The fraudster convinces the victim to send money, assets, or personal information under false pretenses.

- The fraudster makes off with whatever the victim sends them.

In many cases, the fraudster uses a story that creates urgency, both to force a rushed decision and to expedite the process of exploiting the victim. Criminals often pose as authority figures from prominent institutions to gain authenticity and motivate victims to behave in the manner they want.

Examples of Wire Fraud (So You Know What to Look For)

The criminal offense of wire fraud has a relatively broad definition, so many different specific acts of fraud fall under this category. It can be difficult to know what schemes and scams constitute wire fraud; in most cases, it’s best to refer back to the elements required to constitute wire fraud. If all 3 elements are there, it’s likely wire fraud.

To help you determine in practice what is and isn’t wire fraud, we explore a few different schemes that count as wire fraud below:

Advance Fee Fraud

In an advance fee scam, a fraudster offers a victim a share of a large sum of money in exchange for a small, advance payment. The fraudster claims they require the up-front payment to access the larger sum, but the victim will receive a reward (money, gifts, loans, etc.) for helping them access their wealth.

Typically, the fraudster claims the money is locked behind legal, tax, or other fees, which they currently don’t have. The specific circumstances of these scams can vary greatly, but the main premise is always the same.

In some versions of the scam, the fraudster will immediately cut off communication after receiving the ‘advance payment.’ In other versions, the fraudster will come up with other barriers to gaining access to their funds and request more money from the victim.

Advance fee fraud is one of the more common confidence tricks, especially online, as there is little barrier to entry and little skill required.

The Nigerian Prince narrative is a classic example of this type of fraud. The fraudster pretends to be a Nigerian prince who is banished or is unable to access his inheritance in his bank account.

He says he requires the victim to retain his millions in trust for him and guarantees significant compensation in exchange. When the victim pays the advance fees to release the funds, the fraudster disappears.

Phishing

Phishing is one of the most popular types of fraud being conducted today, in part because it’s extremely easy to carry out. Almost anyone can perform this type of fraud with very little expertise, experience, or investment.

In phishing scams, fraudsters don’t actually request money directly from victims. Instead, they trick victims into providing confidential information, which they can then use to commit fraud.

This can be used to steal from the victim directly, but it can also involve identity theft using the victim’s identity.

Phishing scams can take many forms, but in most cases, they are emails that are sent out en masse in the hopes that certain recipients fall victim. These communications may come in the form of a phony email that alerts the victim that their banking password has expired.

The email will contain a link to an illegitimate site where the victim can change their password. However, the link is false and is only used by the fraudster to collect the victim’s information.

Phishing scams are considered wire fraud because the malicious actor uses false pretenses to trick victims to commit fraud intentionally, and it’s being done using wire communications.

Hiring/Job Scam

Much like phishing scams, hiring and job scams are prevalent because they are easy to carry out. Users only need to create a fake employer profile on a job listing site, and they can take advantage of people looking for work.

Fraudsters create fake profiles on job websites and share fake job listings. Victims submit applications - often with a litany of private details - to the fraudster. The fraudster then uses this information to commit fraud through account takeover, identity theft, and other means; if they don’t want to do this themselves, they sell the information to other fraudsters who do.

Hiring and job scams are considered wire fraud because the fraudster uses electronic communications to exploit their victims. Usually, these fraudsters use fake profiles on legitimate job posting sites, but they can also use private communication (such as email, phone, text messages, or video calls) to set up and conduct interviews.

Telemarketing Fraud

Telemarketing fraud is any fraud conducted over the telephone. Typically, it involves fraudulent selling, where fraudsters employ deception to trick victims into ‘buying’ a product or service online.

It’s one of the most common ways that individuals’ money or financial information is fraudulently obtained via wire. It’s extremely easy to conduct, as criminals only need a victim’s phone number to carry it out.

While some versions involve targeted calling, fraudsters typically randomly call numbers, posing as telemarketers from various industries, such as insurance, banking, and even law enforcement.

Some methods are more aggressive than others; for example, some callers claim to be law enforcement and state that they have a warrant for your arrest. They demand that you either pay a fee to avoid a penalty or request personal information in relation to the crime.

In more tame versions, they may claim to be an internet provider calling to check in on services, simply requesting a few details about your service, residence, and payment methods. Either way, they’re using deception to separate victims from their money.

How to Prevent Wire Fraud

Given how popular and broad wire fraud is, it’s extremely challenging for financial institutions to detect and prevent it. Fortunately, there are a few strategies for detecting and preventing wire fraud that FIs can deploy.

1. Train customers on how to keep themselves safe

Frankly, since an abundance of fraud actually falls under the category of wire fraud, it’s rather difficult for financial institutions to detect. A primary component of any sound anti-fraud program should be training customers on how to protect themselves from wire fraud.

Below are some things organizations should train their customers on to help them avoid falling victim to wire fraud:

- Keep personal information private and protected, and refrain from sharing it on publicly accessible websites and platforms.

- Use multi-factor authentication and other enhanced security options with your account for an added layer of protection.

- Use spam filters and call screening to limit your exposure to fraudulent messages in the first place.

- Verify that correspondence is coming from a legitimate channel by researching the company's communication policy and channels. Always verify an email domain or phone number matches the official website.

2. Monitor new accounts as part of onboarding

Fraudsters are most likely to commit fraud immediately after onboarding; taking advantage of quick access and making a getaway before they can be tracked down.

Perform diligent customer onboarding that follows best practices for KYC and identity verification. But don’t stop there; develop specific rules that let you understand the behavior of new accounts.

Monitor to make sure that these accounts aren’t vulnerable to account takeover fraud, and analyze behavior to make sure it aligns with both the business purpose of the account and the expected behavior of the user.

Not all anomalies will amount to fraud, but with proper detection solutions in place, you can catch instances of fraud while they’re happening and stamp them out.

3. Monitor transactions for abnormal behavior

Fraudsters often exploit victims quickly, and limit the number of transactions to avoid raising suspicion. This falls a bit short of a pattern, making this type of fraud hard to detect to the untrained eye.

Prioritizing alerts for abnormal behavior will be incredibly useful, as this will alert teams when a victim is making a suspicious transaction. Transactions that exceed certain thresholds can be escalated to an investigation, allowing risk teams to catch - and in some cases, prevent - wire fraud. Transaction monitoring is one of the best tools for organizations looking to detect - and fight - wire fraud.