Insurance Compliance Requirements (+ the Consequences of Non-Compliance)

Compliance in the insurance industry is difficult to manage — different rules apply based on the jurisdiction, product offerings, and more. State and federal laws need to be considered, as well as international standards that make it easier to deal directly with international customers.

There are also two main facets of compliance to consider: consumer data protection and anti-money laundering (AML) regulations. Both are pivotal in maintaining compliance in the insurance industry.

We’ll explore what insurance companies need to know to manage compliance operations, with a heavy focus on AML compliance (that is what we specialize in after all!). To help insurance companies stay compliant in a constantly changing environment, we cover the following:

Read on to find out more about what insurance compliance really is, the regulations and requirements organizations need to be aware of, and how to build a robust compliance framework.

Insurance compliance refers to the internal controls, processes, and procedures insurance companies use to manage risk associated with regulatory compliance. For most insurance companies, this involves compliance related to money laundering and storing private, personal information of customers.

Insurance compliance regulations are designed to protect consumers — and the overall insurance market. They provide guidelines on how insurance companies need to operate, and set standards they need to follow that keep customer information secure from threats like money laundering and fraud.

Licensing Requirements for Insurance Compliance

Insurance companies — and individual insurance agents — must be licensed to sell insurance. Licensing is regulated at the state level, and most insurance regulations come from state authorities. Licenses need to be renewed periodically to ensure insurance firms and brokers are operating within compliance requirements.

Insurance approved to conduct business within a specific state are domestic insurers of that state. They can then apply for licenses in other jurisdictions as foreign insurers. The application procedure is often accelerated due to reciprocal agreements between states.

With state and federal regulations to be aware of — as well as which ones supersede the other — managing compliance in the insurance industry can be a bit chaotic. To help bring order to this chaos, we explain what regulations apply to insurance companies and the main regulatory agencies responsible for implementing these rules.

State Regulations

Under the McCarran-Ferguson Act, in the United States, each state is responsible for autonomously governing its own insurance industry and markets.

Essentially, the act establishes that Congressional regulations applicable to the business of insurance will not preempt state laws or regulations applicable to the business of insurance. In other words, the industry is first subject to state regulations, and then — when no state law applies — they are subject to applicable federal laws.

National Association of Insurance Commissioners

The National Association of Insurance Commissioners (NAIC) is a U.S. body composed of the chief insurance regulators from the 50 states, the District of Columbia, and the five U.S. territories. As an organization, it’s responsible for setting regulatory standards and offering support and guidance to insurance companies.

The NAIC and state insurance authorities work together to establish guidelines and industry standards and collaborate on regulatory oversight and reviews. Each state determines whether to adopt a specific NAIC rule while also having the option to change the implementation procedure as per jurisdiction requirements.

International Association of Insurance Supervisors

The International Association of Insurance Supervisors (IAIS) is a non-profit, voluntary membership organization responsible for setting international standards for the insurance sector. Its objective is to maintain the fairness and security of insurance markets through effective supervision of the insurance sector.

To achieve this, the IAIS develops principles, standards, guidelines, and best practices for establishing proper supervision of the insurance sector.

The IAIS was established in 1994, and with members from over 200 jurisdictions (that constitute 97% of the world’s insurance premiums) it has a wide reach of influence. It’s arguably the closest thing to a global standard for the insurance industry.

When providing insurance services, insurers must adhere to a set of regulations. Companies are required to respond to disputes in a reasonable period. State regulations aim to safeguard customers from fraudulent insurance practices within the insurance sector by implementing severe penalties and legal accountability for non-compliance.

This is especially true in the insurance industry, where financial, medical, health, and other personal information is being exchanged in detail; significantly increasing the personal — and organizational — risk associated with operations.

Below, we cover some of the main consequences of non-compliance in the insurance sector:

Fines and Penalties

Non-compliance with prescribed regulations can result in hefty fines and punitive damages, which can greatly affect the company or provider’s finances. It is imperative for providers to ensure they onboard legitimate customers, monitor activities, and conduct due diligence to avoid such situations.

Sanctions

Monetary penalties aren’t the only things insurance providers face when failing to meet compliance standards. These companies can also be sanctioned, and subsequently restricted from conducting business.

These sanctions range from minor monetary penalties, to serious regulatory and disciplinary actions, such as license suspension. License suspensions would severely limit an insurance company's service offerings, and make it exceedingly challenging to conduct business effectively.

Reputational Losses

Reputational damage is one of the biggest — and longest-lasting — consequences of non-compliance. It’s particularly devastating because it’s often difficult to repair your reputation and regain the trust of consumers. Sure, you’ll lose some customers in the short term, but some customers will never return to your business — no matter how much you do to rectify the situation.

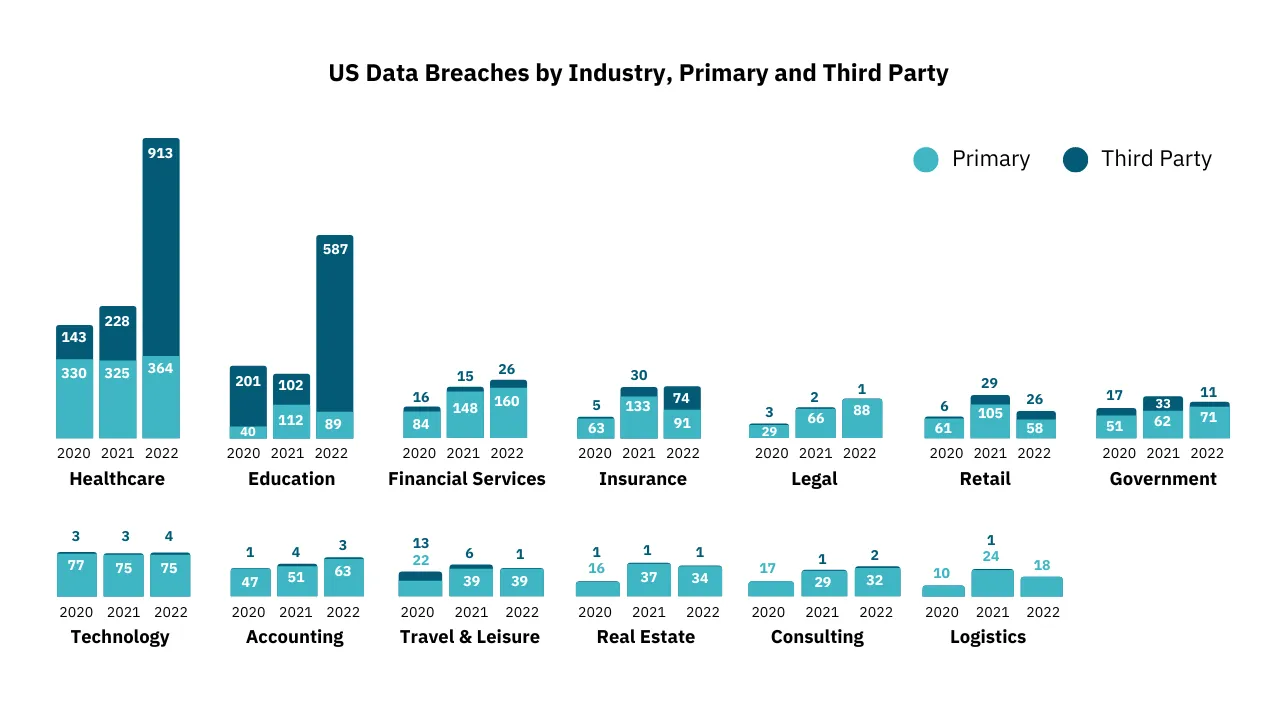

Data Breach

Insurance companies retain extremely personal and sensitive information about their customers, such as financial, medical, health, and other personal details. For fraudsters, this is a treasure trove of personal information that can be used to commit fraud or be sold online. Because of this, insurance companies are direct targets of fraudsters looking to collect personal information that can be used to commit fraud schemes.

Compliance requirements are designed to set standards that help mitigate the risk of data breaches, keeping organizations — and the user information they store — safe. Data breaches can have serious reputational implications, and can lead to severe penalties if proper compliance procedures were not in place and followed.

It also exposes private, personal information and puts users at risk of becoming fraud victims.

Financial Losses

There is one, final cost associated with compliance failures, and that’s financial losses associated with inadequate protections. Even if an organization is never fined for non-compliance practices, they are ultimately cheating themselves, enabling fraudsters to exploit a weak system when it comes to anti-money laundering and fraud prevention.

While there are costs associated with maintaining compliance, these pale in comparison to the potential fraud losses from a system that fails to prevent fraud and money laundering.

Effective insurance compliance demands a rigid program that considers all the elements — including proper consumer data protection and effective AML compliance.

Surprisingly, insurance companies are prime targets for money laundering — and organizations need to be diligent in their anti-money laundering efforts. For this reason, insurance organizations need to adhere to strict compliance regulations.

Below, we explain how organizations can do this.

Set the Tone Throughout the Organization

Compliance operations and efforts aren’t effective when risk and compliance teams operate in a silo from the rest of the organization.

Instead, it’s essential to get stakeholders from other departments involved. This is especially true of the product development team, so that compliance teams can help ensure compliance is easier to achieve based on how the final product works. Product and risk teams — and other departments — should be in contact throughout the design and development stages for the best final results.

Compliance should be an organizational effort, not just that of the risk and compliance team. The tone should be set from the top, and stakeholders from each department should be involved.

Identify and Assess Non-Compliance Risks

It’s essential that the tone for compliance operations is set at the top, and that a proper program is established that allows teams to effectively manage risk. To do this properly, organizations need to identify and assess compliance requirements — as well as any non-compliance risks that come with that.

It's crucial to carry out an internal gap analysis to identify the company's risks related to compliance. Ensure teams monitor all applicable state and federal regulations that apply to both your industry and company (based on the services you provide). This is critically important when devising your compliance program, but it’s also important to revisit this over time and make sure you’re aware of all potential compliance changes you need to follow.

Understand not only what compliance guidelines you have to follow, but the risks associated with compliance failures and breaches.

Compartmentalize Different Types of Compliance

Companies operating in the insurance industry are subject to two main compliance regulations — consumer protection laws related to data security and anti-money laundering regulations that prevent money laundering efforts by criminals.

Each is important and has to be followed, but each has its own specific elements to consider when managing compliance. It’s best to have a solution that allows you to manage all of these different compliance operations in one place, while still being able to compartmentalize each type to make it easier to effectively manage.

Larger teams can have dedicated team members that handle each type of compliance, but still work together to implement best strategies across the board.

Establish a Clear Policy, and Make it Accessible

Develop a clear, written policy that defines the organization's compliance program. It should outline the principles, processes, and procedures that need to be followed by team members.

Make it easily accessible to all staff so that it can easily be referenced as team members need it. Ideally, team members can use this policy as a source of truth for conducting compliance operations, down to the exact procedures they need to follow. Provide training during onboarding and periodically review staff to refresh them.

Use an AML Compliance Management Solution

Anti-money compliance processes and procedures can be done manually, but they’re significantly time-consuming and resource-intensive. Fortunately, AML compliance management solutions help with this significantly — optimizing workflows and processes to save time and improve efficiency.

When using the proper solution, they streamline the entire AML compliance process, from performing identity verification all the way through to SAR reporting. With information accessible from a unified dashboard, it’s extremely easy to manage your entire AML compliance operation.

Reevaluate and Update Your Compliance Systems and Program

There are a number of insurance compliance regulations to consider based on a number of variables, such as the jurisdiction, the industry, and the actual product offerings of the company. Compliance regulations are also constantly changing and advancing, making them hard to keep up with.

Systems will need to be updated regularly — this will be a continuous and constant cycle to ensure compliance is always up-to-date. But systems aren’t the only thing that needs to be updated; insurance companies also need to review and update their compliance program to keep pace with regulatory compliance changes in the industry.

Compliance teams need to know what regulations are relevant, what applies, and what changes need to be made to stay compliant.

Perfect Insurance Compliance with Unit21

By nature, insurance companies of all types require a lot of personal information from customers. This makes consumer protection and data security compliance a core component of operations — personal information needs to be stored and managed securely and safely. And in today’s day and age, there are a lot of applicable laws, both state (like the CCPA) and federal.

But another major component of insurance compliance is AML compliance — which prevents money laundering from occurring and protects both customers and the company. The fact is, criminals will look for any avenue to launder their money, and the insurance industry is no different.

It’s best to use a combination of customer onboarding to verify customers are who they claim to be and transaction monitoring to analyze premium payments for anomalies. Risk and compliance teams can leverage these systems to keep money mules and other criminals off their platform and detect any suspicious activity that gets through by screening — and analyzing — customer transactions.

Schedule a demo to learn how Unit21 can help your insurance company streamline AML compliance operations to keep your organization safe from criminals.