Electronic Funds Transfer (EFT)

Advantages & Common Payment Methods

These days, money is often moved completely digitally without any physical cash, checks, or financial employees involved. This class of transaction is called an EFT, or electronic funds transfer.

Here, you’ll learn what EFTs are, how they work, what some of the common types are, and how they are regulated through the Electronic Funds Transfer Act (EFTA).

What is Electronic Funds Transfer (EFT)?

An electronic funds transfer is a class of transactions in which money moves from one financial account to another entirely digitally. These transactions can be within the same financial institution or different financial institutions, and do not require paper documents or bank employee involvement.

You’ll commonly hear the term “EFT payment,” as EFT technology typically involves making and processing payments. However, not all EFT transactions are “payments” in the strictest sense of settling a debt.

For example, they could be used to move money between two bank accounts owned by the same person or used to send money as a gift to family members. There are many types of EFT transactions, some of which we’ll cover later.

Electronic Funds Transfer Act (EFTA)

The EFTA is a US law designed to protect people when they shop or perform banking transactions via EFTs. The Electronic Funds Transfer Act is also known as Regulation E of the Federal Reserve Board.

When was the Electronic Funds Transfer Act Signed Into Law?

The Electronic Funds Transfer Act was signed into law in the US in November of 1978 by President Jimmy Carter.

What is the Purpose of the Electronic Funds Transfer Act?

So what does the Electronic Funds Transfer Act do? Basically, it outlines the rights and responsibilities of financial institutions and their customers when it comes to conducting EFT transactions.

For instance, financial institutions must inform a customer what they may be liable for if their payment card is lost or stolen. This must include a description of how the institution will help the customer resolve this problem, along with dedicated contact information (usually a phone number) to a department for reporting lost or stolen cards.

Under the EFTA, customers are also absolved of at least some liability for unauthorized transactions (including those initiated with a lost or stolen credit/debit card) if they notify their bank within specific time frames. In addition, banks must limit the amount of money that a person can withdraw using their debit card each day. This helps to protect customers from having funds drained from their accounts by large and/or repeated withdrawals, especially unauthorized ones.

How Does Electronic Funds Transfer Work?

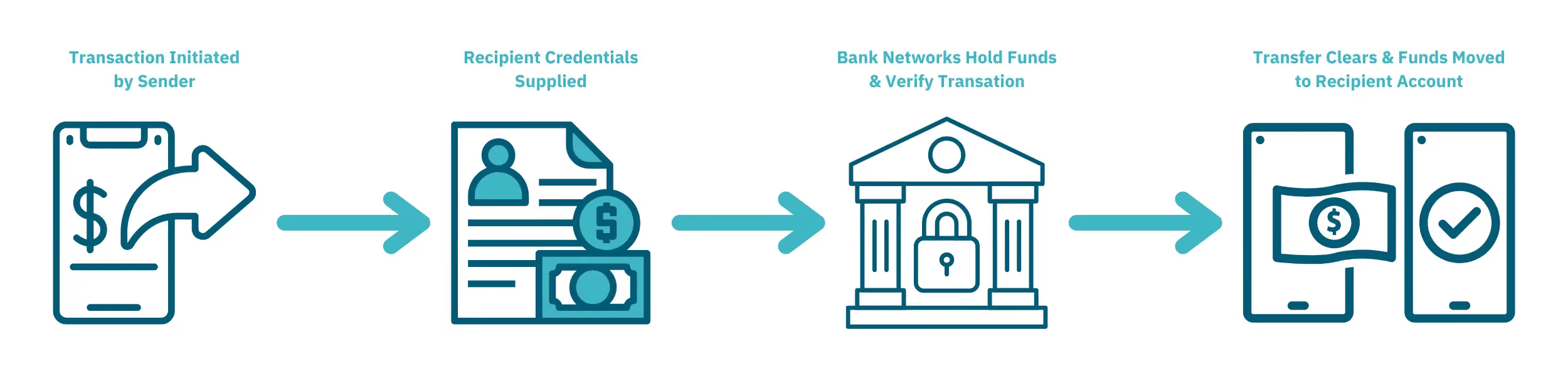

So how does an EFT payment work? It’s fairly straightforward, and generally requires five things: a sender, the sender’s financial information, a receiver, the receiver’s financial information, and one or more digital banking networks to handle the transaction.

An electronic fund transfer process looks something like this:

- The sender initiates the transaction, using their financial credentials to authorize it.

- The sender supplies the receiver’s credentials (bank name, account type, account number, routing number, etc.) to specify which account they will send money to.

- The digital banking networks involved usually hold the transaction briefly if it needs to be reversed, including if it’s deemed suspicious.

- If everything is valid, the transfer clears, and the money is moved from the sender’s account to the recipient’s account.

Advantages of Electronic Funds Transfer

Electronic fund transfer systems have become increasingly popular methods of doing business. This shouldn’t be a surprise when considering their advantages over transactions that use physical money. For instance:

- Speed: Though they can sometimes take up to a few days to clear payment networks, EFTs are generally faster than sending cash or checks through the mail.

- Flexibility: Many forms of EFTs can be done online, enabling business to be conducted pretty much anywhere. A person doesn’t necessarily need to visit an actual store or visit a bank to withdraw money or conduct other banking transactions.

- Automation: EFTs can be programmed to occur at specific intervals. This allows for making recurring payments without having to repeatedly withdraw cash, write checks, or worry about payment deadlines.

- Cost: Transactions via cash or check involve several expenses. These include printing checks or bills, paying for postage, and sometimes paying for an employee to handle the money. EFTs avoid most of these, making them a cost-effective solution.

- Less human error: Cash or check transactions can be prone to human error. Someone may miscount or miscalculate the amount of money to be transferred, or they may lose track of the cash or check in transit to where it’s supposed to go (especially through the mail). EFTs significantly lessen these risks because they’re handled mainly by computers.

- Security: Because EFTs verify and move money electronically, they involve less risk of theft or counterfeiting than when dealing in cash and checks.

Types of Electronic Funds Transfer: Common EFT Payment Methods

EFT is a blanket term that refers to many different types of transactions that happen at least partially electronically, without physical money changing hands between actual people. So an electronic funds transfer example isn’t too hard to find. Here are some that happen daily.

Electronic Check

In place of a paper check, this method involves a person giving a merchant the information that would typically be on a check. Then the merchant can, on the person’s authorization, create a virtual check and accept it as payment.

Direct Deposit

A payer uses a payee’s banking information to send money directly to the payee’s bank account at specified intervals. This is typically used by employers to pay their employees without using paper checks. It can also be used for recurring payments (such as for utilities), or paying off large debts in installments.

In the US, direct deposit often goes through the Automated Clearing House (ACH) system, which processes transactions in batches. So when it comes to electronic funds transfer vs. ACH, payments that go through the ACH are a type of EFT: money is moved electronically between accounts, with minimal paperwork or human involvement. However, not every EFT transaction involves the ACH; some are processed sooner (even immediately).

Automated Teller Machines (ATMs)

These are electronic kiosks that a person can use to withdraw, deposit, or transfer money. The appropriate accounts at their financial institution are electronically debited (or credited), without the person needing to actually enter a bank.

Credit and Debit Cards

Many people now use payment cards instead of cash at points of purchase. By swiping, dipping, or tapping a card on a reader, the reader collects a customer’s banking information and authorizes a withdrawal of funds to pay for the items or services bought.

Pay-by-Phone

Similar to electronic checks, this involves a person giving a merchant their banking information over the phone to authorize a payment from the person’s account. It can also involve a person phoning their bank to move money between accounts or authorize bill payments.

Wire Transfers

The term “wire transfer” typically refers to the electronic transfer of money between banks, either domestically or internationally. They generally allow large sums of money to be moved in a short amount of time but can be expensive in terms of fees. They also usually can’t be canceled once they’re initiated.

The difference between electronic funds transfer vs. wire transfer is simply that wire transfers are a specific type of EFT, similar to ACH payments.

Online Shopping and Banking

Many shopping and banking transactions can now be done virtually anywhere over the internet. Like with other forms of EFTs, customers provide their banking credentials ahead of time or as authorization. Then they can pay for goods or services purchased, pay bills, move money between accounts, and so on without handling any physical money.

Process EFTs Securely with Help from Unit21

Though the advantages of electronic funds transfer have helped make the practice very commonplace nowadays, it is still vulnerable to financial crime. Some EFTs are difficult to trace or reverse, particularly wire transfers and those involving ATMs. And they can happen so quickly that a criminal can get the money and use it before authorities or financial institutions can react.

So the best solution is to prevent fraud before it happens by monitoring EFT transactions with suspicious characteristics. Find out how Unit21 can help with this process by booking a demo with us today.