First-Party Money Mules: The Hidden ACH Laundering Threat

ACH rails have become a preferred pathway for money laundering, but not always in ways institutions expect.

One growing and often underestimated risk is first-party money mules, where real customers, or even carefully constructed synthetic identities, may unknowingly or deliberately participate in laundering activity.

As NACHA 2026 approaches, financial institutions can no longer rely solely on traditional fraud detection; first-party money mule activity is now squarely on the radar.

What Is a First-Party Money Mule Activity?

A first-party money mule is a fully onboarded Identity who passed KYC involved in laundering, either:

- Willingly, often recruited to move funds for a criminal organization, or

- Unknowingly, tricked into receiving and forwarding money through their legitimate account.

These individuals often have legitimate relationships with the financial institution and have passed identity verification and KYC checks.

How ACH Is Being Used for Layering

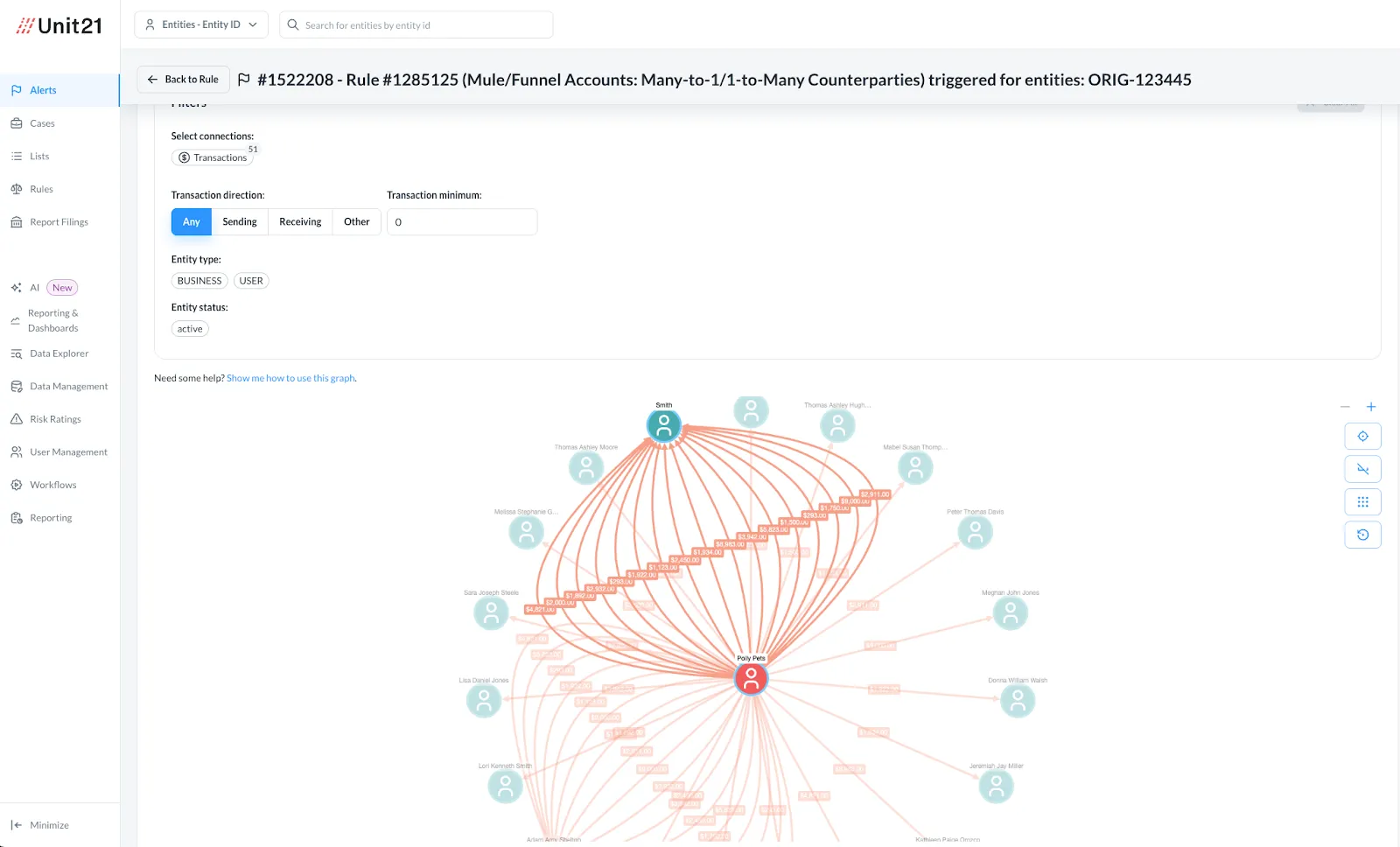

First-party money mules often play a key role in layering, the stage of money laundering where criminals move and disguise funds to obscure their origin.

They use ACH rails to send small-dollar, high-frequency transfers, quickly shift money between institutions, and reroute it through multiple sleeper accounts, creating a trail that looks ordinary on the surface but is designed to hide where the money truly came from.

Example flow:

An initial transfer lands in one account → layered through three mule accounts → eventually sent to crypto or offshore accounts.

Visual aids like simple flow diagrams or narrative walkthroughs can make these layering schemes easier for teams to grasp and monitor.

Why Detection Is So Difficult

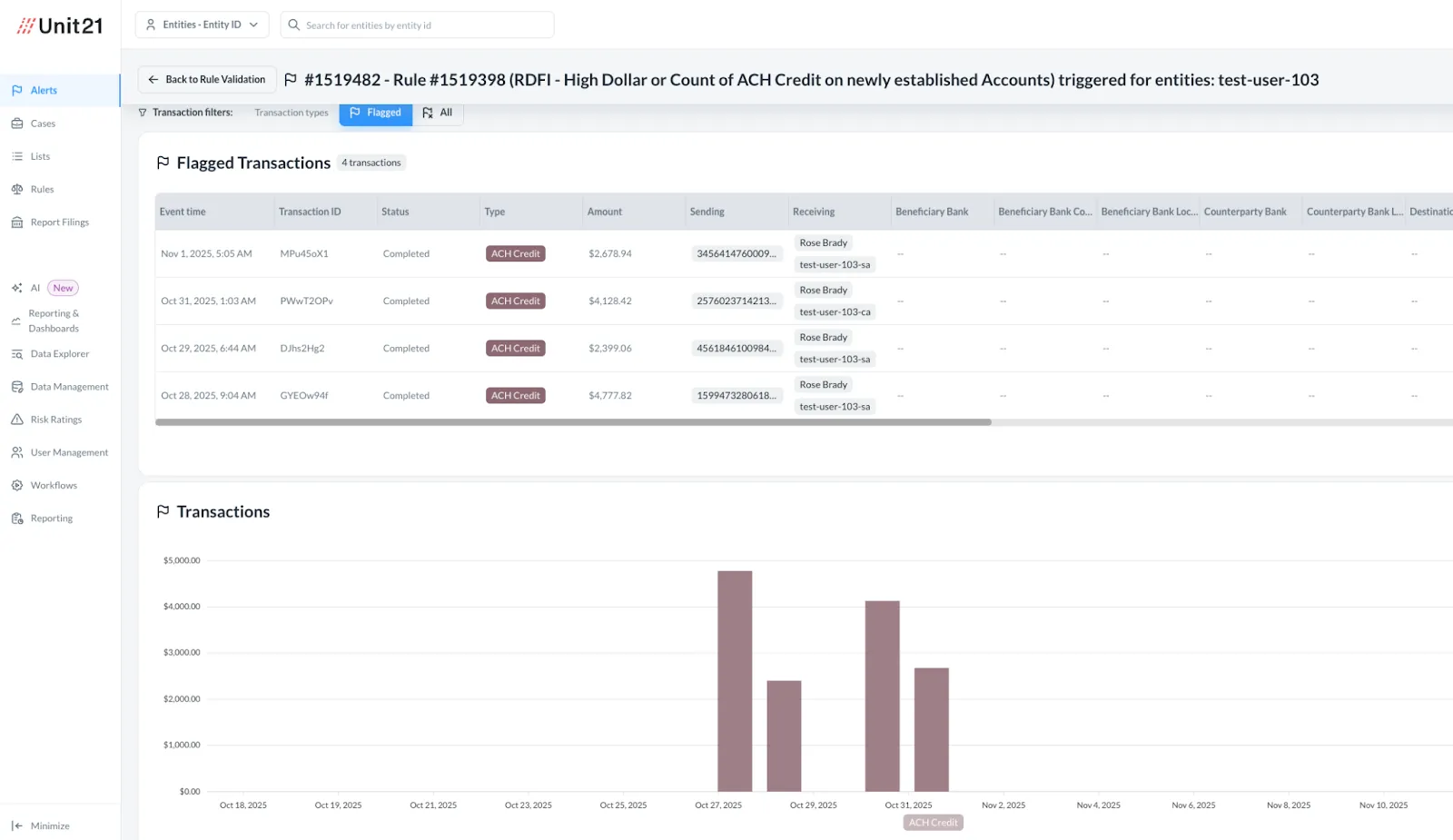

Detecting a first-party money mule activity is challenging because, on the surface, these accounts look completely legitimate. They pass KYC checks without issue, generate no fraud chargebacks to draw attention, and often move money in patterns that resemble normal customer behavior.

Unless you’re watching for subtle shifts in velocity, unusual counterparties, or quiet routing patterns across ACH rails, their laundering activity blends in almost perfectly with everyday account use, which is exactly why so many institutions miss it.

NACHA 2026’s Risk Implications

NACHA’s 2026 changes highlight institutional liability for laundering activities that occur through legitimate accounts. Ignoring first-party money mule activity could signal weak oversight or even regulatory negligence. Auditors will evaluate pattern detection, control sophistication, and proactive monitoring, rather than just looking at losses.

What regulators will expect FIs to monitor more closely in 2026:

- Risk segmentation: Not all accounts should be treated and monitored the same way

- Patterns of unusual fund movement across ACH rails

- Accounts showing rapid inflows and outflows with no clear purpose

- Repeated exposure to known mule accounts or high-risk counterparties

- Weak or inconsistent monitoring of first-party behaviors that can mask laundering

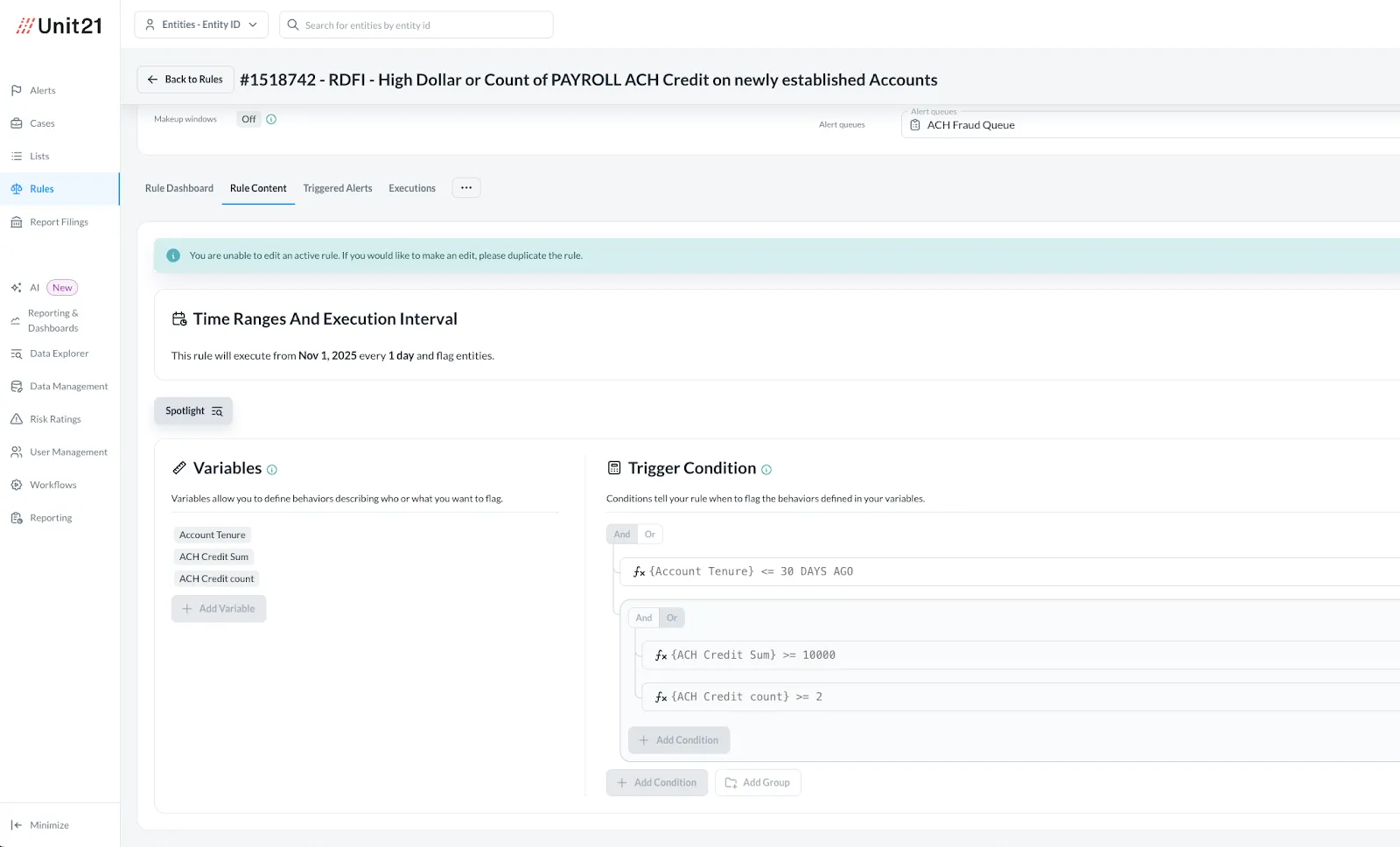

Building Detection Capabilities That Work

Financial institutions need advanced tools to catch subtle, networked money mule activity. Effective detection often relies on:

- Network/graph analysis: Reveals mule rings and shared counterparties

- Anomaly detection: Spots unusual transaction velocity, frequency, and routing

- Behavioral analytics: Flags activity outside segment-normal behavior

What detection should flag:

- Same-day high-value inflows and outflows

- Transfers to unrelated or high-risk accounts

- Repeated exposure to known mule accounts

How Unit21 Supports This Typology

Unit21 gives financial institutions a clearer way to spot first-party money mule activity by combining transaction monitoring with powerful network analysis. Teams can quickly see how accounts, devices, and counterparties connect, even when the activity looks normal on the surface. And because the system is fully customizable, rules can evolve as mule behaviors change.

With this level of visibility, fraud and risk teams can catch laundering patterns early, long before they become regulatory or financial issues. It’s a smarter, more proactive way to stay ahead of emerging ACH threats.

Ready to Close the Gap on First-Party Money Mules Risk?

First-party money mules are one of the most overlooked threats in ACH fraud, and with NACHA 2026 raising the bar, financial institutions can’t afford blind spots. Strengthening detection now not only reduces your exposure but also signals true control maturity to regulators.

If you want to understand how your current fraud defenses stack up, schedule a free fraud detection session with Alex today and get a clear roadmap for staying ahead of emerging money mule activity.

Alex Faivusovich is a fraud prevention leader fighting financial fraud for the past 16 years. His career started in Israel at Leumi Card (MAX), culminating in him leading a team of 15 fraud analysts. In the U.S., Alex joined Matrix-IFS as a senior fraud consultant, providing expertise for Tier -1 banks and Fintech programs.

Alex later served as the Head of Fraud Risk at Lili Bank, leading the implementation of fraud prevention technology within the company and owning the risk policy for first—and third-party fraud. Today, Alex is Head of Fraud Risk at Unit21, guiding and advising clients along their fraud prevention journey.