2026 Nacha Rule Changes: FAQs for Financial Institutions + Key Effective Dates

This year, the Nacha operating rules are getting an important update. The 2026 Nacha rule changes are designed to reduce fraud and false-pretense payments across the ACH network. These updates affect financial institutions, non-consumer originators, Third-Party Senders (TPS), and Third-Party Service Providers (TPSPs).

Below is a practical overview of the rule changes and FAQs to help compliance, fraud, risk, and operations teams understand what’s changing, who is impacted, and how to prepare.

2026 Nacha Rule Changes Overview

What are the Nacha 2026 ACH Operating Rules?

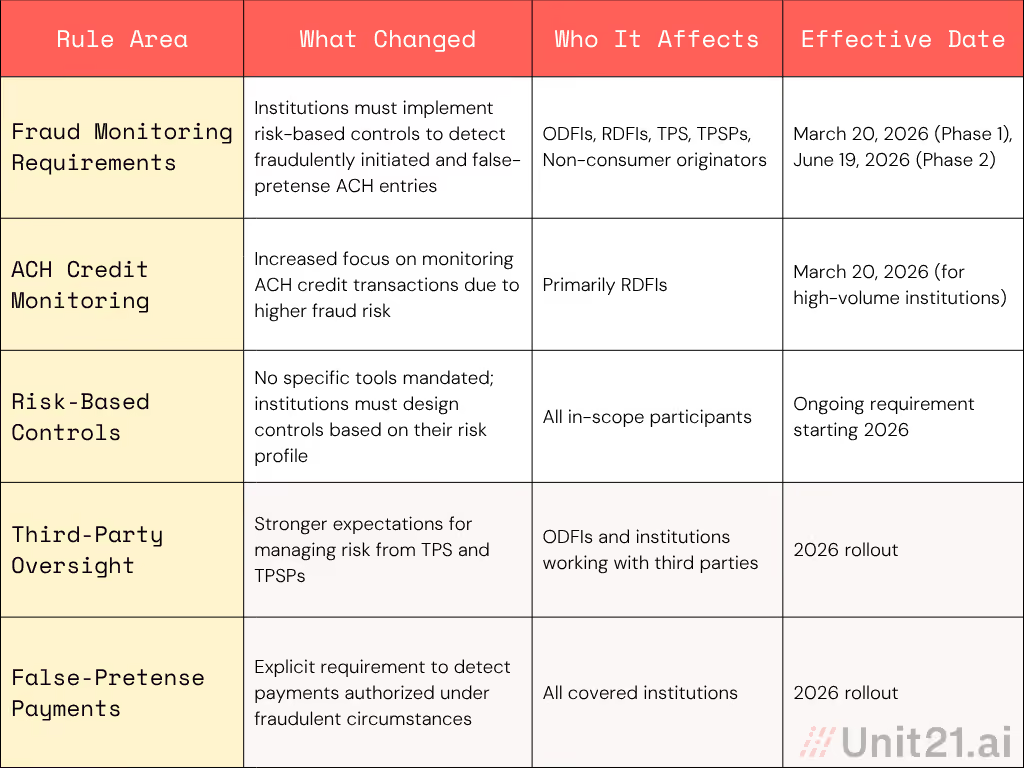

The Nacha 2026 ACH operating rules require certain ACH participants to implement risk-based procedures to detect and prevent fraudulently initiated and false-pretense ACH entries. These updates are part of Nacha’s broader effort to strengthen ACH network risk management, particularly as fraud schemes increasingly target ACH credit transactions.

Ready for the 2026 NACHA changes? Move from rule interpretation to execution with a practical fraud monitoring checklist designed for compliance and fraud teams.

Download the NACHA Fraud Monitoring Checklist

When do the 2026 Nacha ACH Operating Rules take effect?

Phase 1 – Effective March 20, 2026:

This phase applies to:

- All ODFIs, Non-consumer Originators, Third-Party Service Providers (TPSPs), and Third-Party Senders (TPSs) that originated 6 million or more ACH entries in 2023.

- RDFIs with 10 million or more ACH receipt volume in 2023, who must comply with ACH Credit Monitoring requirements.

Phase 2 – Effective June 19, 2026:

Applies to:

- All remaining in-scope participants, regardless of ACH volume.

These updates require the implementation of risk-based procedures to detect fraudulently initiated and false-pretense ACH entries, with increased attention to ACH credits due to their vulnerability to fraud schemes.

Who is required to comply with the 2026 ACH Operating Rules?

The Nacha ACH rules apply to several participants in the ACH ecosystem, including:

- Originating Depository Financial Institutions (ODFIs)

- Receiving Depository Financial Institutions (RDFIs), particularly for ACH credit monitoring

- Non-consumer originators

- Third-Party Senders (TPS)

- Third-Party Service Providers (TPSPs)

Applicability depends on an institution’s role in ACH processing and, in some cases, transaction volume. Read more about how ODFIs, TPSs, and TPSPs must evolve for NACHA 2026 rule changes.

What is required under the new Nacha Operating Rules?

Under the 2026 updates, covered institutions must put risk-based controls in place to prevent ACH fraud and false-pretense payments. This typically includes:

- Implementing risk-based monitoring procedures

- Identifying fraudulently initiated ACH entries

- Detecting false-pretense payments

- Monitoring ACH credits, with specific obligations for RDFIs

- Maintaining oversight of third-party ACH relationships

Nacha does not mandate specific tools or thresholds. Institutions are expected to design controls that are appropriate for their risk profile.

What are “false-pretense” ACH payments?

A false-pretense ACH payment occurs when a legitimate user is deceived into authorizing a payment under fraudulent circumstances, such as impersonation scams, payroll redirection fraud, or business email compromise. While these payments are technically authorized, they are still fraudulent, which makes them more difficult to detect using traditional fraud rules alone.

Do the Nacha ACH rules apply to credits or debits?

The 2026 Operating Rules apply to both ACH debits and credits, but there is increased focus on ACH credits, including payroll payments, vendor payments, and payouts or disbursements. ACH credits are frequently targeted through social engineering and mule activity, which is why the rules explicitly address RDFI monitoring responsibilities.

What are Third-Party Senders (TPS) and TPSPs?

Under the Nacha Operating Rules, financial institutions are responsible for managing the risk introduced by third-party ACH relationships.

- Third-Party Sender (TPS): An entity that originates ACH entries on behalf of another party, such as payroll processors or payment facilitators

- Third-Party Service Provider (TPSP): A company that provides ACH-related services but does not originate entries itself

What is a mule account in ACH fraud?

A mule account is used to move funds on behalf of a fraudster and often shows activity that does not align with the account’s stated purpose. Common indicators include:

- High transaction velocity

- Rapid inflows followed by quick withdrawals

- Inconsistent or erratic transaction behavior

- Name mismatches across ACH entries

Mule accounts are a major source of ACH fraud under the Nacha 2026 rule changes. Learn more about money mules.

How should financial institutions identify mule accounts?

Effective mule detection relies on a risk-based approach, including:

- Behavioral transaction monitoring

- Velocity and pattern analysis

- Network and relationship analysis

- Monitoring ACH credit activity across accounts

Because mule activity often appears authorized on the surface, context and behavior analysis are critical.

Are institutions required to share data under the Nacha rules?

No. The Nacha 2026 ACH Operating Rules do not require data sharing or participation in fraud consortiums. That said, some institutions choose to use privacy-preserving consortium intelligence to enhance detection, as long as customer data remains protected.

Are there privacy concerns with ACH fraud monitoring?

Privacy remains a key consideration. Any ACH fraud monitoring program should minimize unnecessary data exposure, use anonymization or hashing where appropriate, and comply with applicable privacy and data protection laws. Many modern fraud platforms now rely on privacy-safe signals rather than raw data sharing.

How can Unit21 help comply with the Nacha 2026 Operating Rules?

Unit21 provides a unified risk and compliance platform that helps institutions operationalize the Nacha Operating Rules by supporting:

- ACH transaction monitoring

- False-pretense payment detection

- Mule account identification

- Risk-based rule creation

- AI-driven anomaly detection

- Privacy-safe consortium intelligence

This approach allows institutions to meet Nacha’s expectations without relying on siloed fraud and compliance tools.

Do the Nacha Operating Rules require specific technology?

No. Nacha does not prescribe vendors or technologies. However, institutions must be able to show that their controls are risk-based, documented, and effective at detecting fraudulent and false-pretense ACH activity. Many institutions adopt modern platforms to meet these expectations efficiently.

What should financial institutions do now to prepare?

To prepare for the 2026 Nacha ACH Operating Rules, institutions should:

- Assess ACH fraud and false-pretense risk exposure

- Review third-party ACH relationships

- Evaluate existing ACH monitoring coverage

- Identify gaps in ACH credit monitoring

- Implement scalable, risk-based controls

Starting early reduces implementation risk and regulatory pressure as compliance deadlines approach.

Prepare for the Nacha 2026 ACH Operating Rule Changes

The Nacha 2026 ACH operating rules represent a shift toward proactive, risk-based ACH fraud prevention, especially for false-pretense payments and ACH credits. Institutions that unify fraud, compliance, and ACH monitoring under a single framework will be best positioned to meet regulatory expectations while reducing fraud losses.

If you’d like to see how Unit21 supports ACH risk monitoring and Nacha compliance, register to watch the webinar or book a strategy session with Alex to discuss your specific use case.

Alex Faivusovich is a fraud prevention leader fighting financial fraud for the past 16 years. His career started in Israel at Leumi Card (MAX), culminating in him leading a team of 15 fraud analysts. In the U.S., Alex joined Matrix-IFS as a senior fraud consultant, providing expertise for Tier -1 banks and Fintech programs.

Alex later served as the Head of Fraud Risk at Lili Bank, leading the implementation of fraud prevention technology within the company and owning the risk policy for first—and third-party fraud. Today, Alex is Head of Fraud Risk at Unit21, guiding and advising clients along their fraud prevention journey.