RDFIs Under Pressure: How to Stay Ahead of NACHA’s 2026 Rule Changes with Unit21

The ACH ecosystem is undergoing one of its most significant regulatory overhauls in years — and this time, Receiving Depository Financial Institutions (RDFIs) are in the hot seat. Unlike a simple payment rail, the ACH network is an interconnected ecosystem involving multiple participants: originators, operators, ODFIs, RDFIs, and third-party processors. While Originating Depository Financial Institutions (ODFIs) have traditionally carried most of the fraud monitoring burden, NACHA’s 2026 Fraud Monitoring Rule expands that responsibility to RDFIs — making them essential players in the fight against ACH fraud.

If you’re an RDFI, you’re no longer just a passive processor of inbound transactions. You’re now a frontline defender — expected to monitor, detect, and act on suspicious incoming ACH activity.

This blog will help you understand how RDFIs are now expected to act, not just receive, and how to detect fraud before funds are withdrawn.

To see how all participants in the origination chain must evolve — and what proactive steps you can take today — explore our NACHA 2026 Educational Hub. You can also read our 2026 NACHA operating rule FAQs for financial institutions.

What Is an RDFI — and Why Does NACHA Now Care So Much?

An RDFI is a financial institution that has agreed to accept ACH transactions under the NACHA Operating Rules. It is the bank on the receiving end of an ACH entry, responsible for posting funds to the receiver’s account.

Historically, RDFIs had minimal monitoring obligations. Their role was largely passive: to post valid entries received from the ACH network, not question their intent or origin.

But starting in March and June 2026 (depending on your transaction volume), that changes.

Here’s what NACHA now expects RDFIs to do:

- Proactively monitor inbound ACH transactions for indicators of fraud.

- Identify anomalous behavior such as unusual transaction amounts, recipient patterns, or mismatched names.

- Initiate returns of suspicious funds without waiting for the ODFI to flag the transaction.

This rule shift is rooted in a growing trend: fraudsters using RDFIs as the endpoint for stolen funds, especially through impersonation-based schemes (e.g., tax refund fraud, unemployment scams, synthetic identities).

The Fraud Risks RDFIs Must Now Catch

With greater visibility into inbound ACH data, RDFIs are uniquely positioned to stop fraud post-origination but pre-withdrawal. Here are two real-world fraud scenarios where the new rules (and Unit21’s platform) make all the difference.

Scenario 1: Payroll Fraud via Synthetic Identity

A fraudster creates a synthetic identity and opens a checking account at your bank. Days later, multiple payroll direct deposits start flowing into this account — but none of them match the identity of the account holder.

With Unit21’s rules engine, RDFIs can:

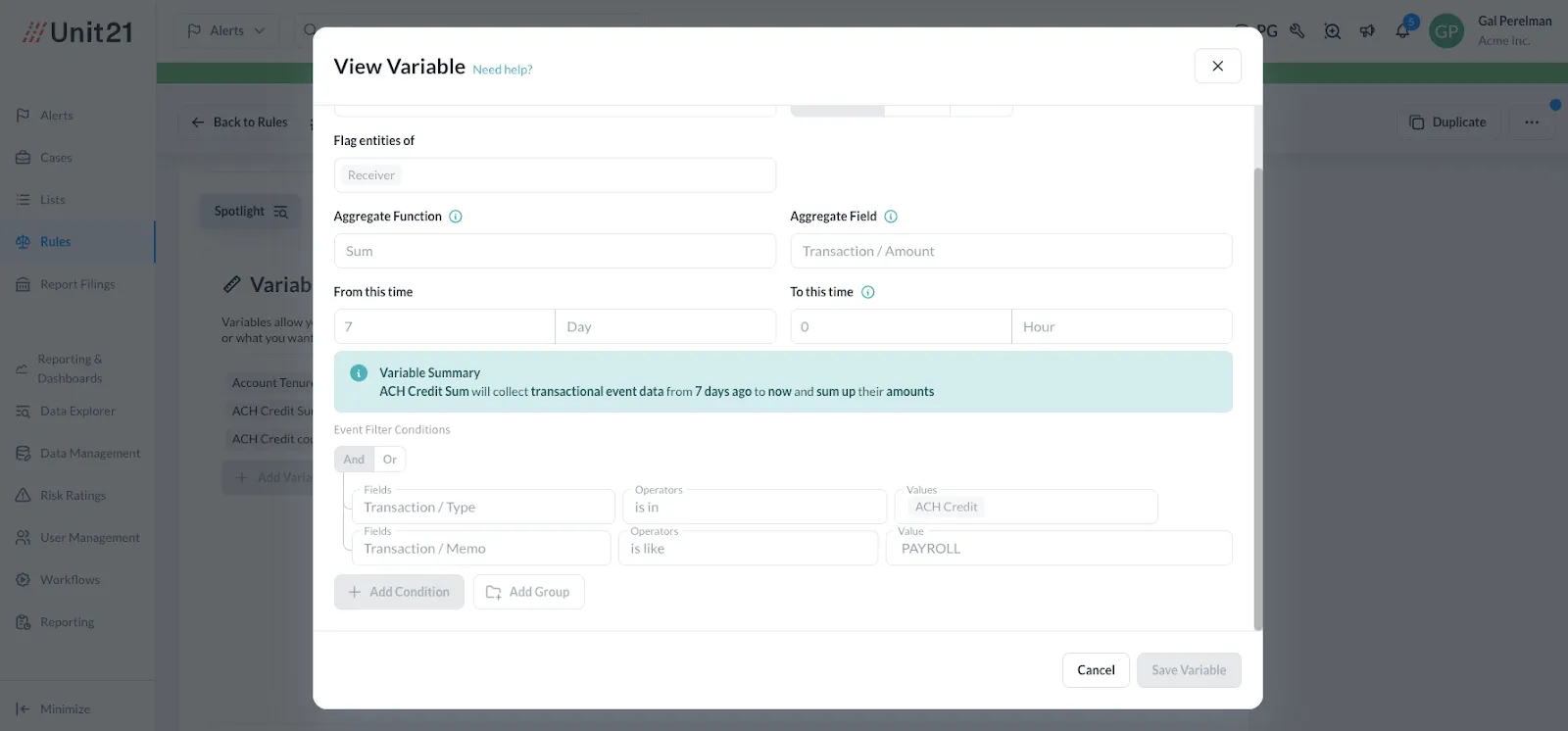

- Detect ACH metadata containing terms like “PAYROLL” or “PURCHASE”.

- Monitor for unusually high deposit velocity (e.g., $25,000 across 3 employers in 48 hours).

- Use fuzzy logic to assess whether the payee’s name matches the account holder.

Outcome: The anomaly is flagged immediately. You investigate, confirm synthetic identity usage, and return the funds before they’re siphoned out.

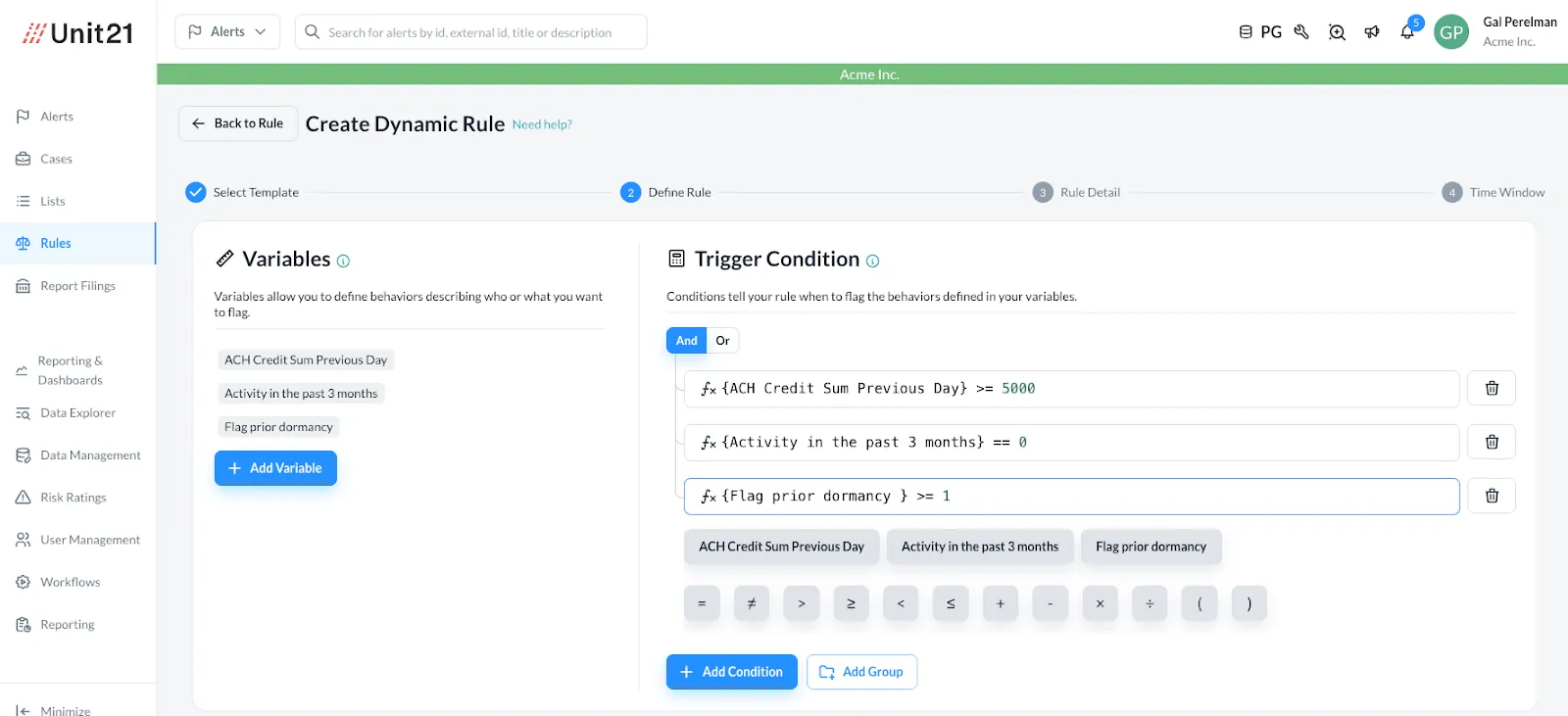

Scenario 2: ACH Tax Refund Fraud + Dormant Account Reactivation

An inactive account on your system suddenly receives an $8,300 IRS refund via ACH. The account’s profile shows a recent address change and a new phone number.

Unit21 automatically flags:

- High-risk keywords like “IRS TAX REFUND” in the ACH memo.

- A dormant-to-active account reactivation pattern: No activity for 90+ days, now receiving a large credit.

- Recent profile changes — often associated with Account Takeovers (ATOs).

With Unit21, you can define your institution’s custom dormancy rules (e.g., 3, 6, or 12 months of inactivity) and set a reactivation event — such as receiving $5,000+ in a 24-hour window.

Outcome: You return the refund before it’s withdrawn and file a Suspicious Activity Report (SAR), staying compliant and minimizing reputational damage.

Scenario 3: Mule Account Linkage via Micro-Deposits

A new account is opened at your institution. Within two weeks, it receives eight micro-deposits from different external banks — often a sign of attempts to link multiple external accounts.

With Unit21, you can:

- Automatically detect accounts receiving more than 6 micro-deposits in a short time window (e.g., 30 days).

- Combine this with rules for new accounts (e.g., established <30 days) to highlight risky behavior early

- Investigate before funds arrive — preventing potential money mule activity before it escalates.

Outcome: You flag the account for review, block further links, and stop incoming fraud before it hits the books.

How Unit21 Future-Proofs RDFIs Against the NACHA Rule

At Unit21, we know that compliance shouldn’t be a blocker — it should be an enabler. That’s why our platform includes out-of-the-box tools built specifically for RDFIs to meet 2026 rule expectations without a massive engineering lift.

1. Flexible Rules Engine (No-Code Customization)

- Build and adjust fraud detection logic via a drag-and-drop interface.

- Create thresholds for velocity, frequency, and unusual transaction descriptions.

- Automate alerts for escalation and resolution workflows.

2. Fuzzy Matching & Entity Resolution

- Automatically flag mismatches between incoming transaction names and account holders.

- Set similarity thresholds (e.g., 70%) to trigger alerts only when needed — reducing noise.

3. Dual Role Monitoring for ODFIs + RDFIs

- Monitor both sending and receiving entities from a unified dashboard

- Detect money mule behavior when an entity is both originator and receiver.

4. Pre-Built RDFI Rule Templates

- Plug-and-play rules to detect payroll fraud, benefit disbursement abuse, and synthetic identity schemes.

- Fully customizable to your institution’s risk appetite and transaction patterns.

Why This Matters Beyond Compliance

The NACHA 2026 rule isn’t just a checkbox — it’s an industry-wide signal: fraud defense now starts and ends with everyone in the chain. For RDFIs, this is an opportunity to:

- Demonstrate regulatory leadership.

- Reduce losses due to unauthorized transactions.

- Improve customer trust and account safety.

Key Takeaways: Why Unit21 Is the Strategic Advantage RDFIs Need

- RDFIs are now responsible for monitoring inbound ACH transactions and returning fraudulently obtained funds.

- Unit21 empowers RDFIs with fuzzy matching, velocity checks, and custom rule-building tools to adapt fast.

- Our platform is ready today to help you meet the 2026 NACHA requirements — with zero code and zero friction.

Ready to Lead the Industry in ACH Fraud Defense?

Explore Unit21’s NACHA Rule Educational Center or sign up for our upcoming Webinar: Navigating NACHA’s 2026 Operating Rules With Unit21, where we simulate real-world attacks and show how RDFIs can stop them.

Alex Faivusovich is a fraud prevention leader fighting financial fraud for the past 16 years. His career started in Israel at Leumi Card (MAX), culminating in him leading a team of 15 fraud analysts. In the U.S., Alex joined Matrix-IFS as a senior fraud consultant, providing expertise for Tier -1 banks and Fintech programs.

Alex later served as the Head of Fraud Risk at Lili Bank, leading the implementation of fraud prevention technology within the company and owning the risk policy for first—and third-party fraud. Today, Alex is Head of Fraud Risk at Unit21, guiding and advising clients along their fraud prevention journey.