The Complete Guide to Regtech (Regulatory Technology)

Fraudsters have—and continue to—come up with many clever ways to commit money laundering and other financial crimes. Most, if not all, exploit weak points in financial institutions’ infrastructures and processes. This has led financial regulators to devise an ever-lengthening list of rules that must be followed to patch these holes.

Unfortunately, with the fast pace of today’s digital society, keeping up with new financial crime schemes—and the regulations meant to block them—is an enormous task. That’s why many FIs are turning to Regtech: technology that helps streamline (and even automate) compliance-related tasks.

This guide will cover in detail what Regtech is, what FIs are specifically using it for, where it helps FIs the most, and what experts are saying to look for in Regtech in the near future.

Let’s first talk about what Regtech is, particularly in comparison to some similar classes of technology.

Regtech refers to technology (and sometimes companies that offer it as a service) that helps companies in regulated industries manage their compliance operations. This includes automating tasks like transaction monitoring, unusual activity detection, and report filing for reviews and audits.

So why is Regtech important? The short answer is that it helps businesses save money on complying with regulatory requirements in their industries.

It does this in two main ways. The first is by automating repetitive compliance processes that take up too much time and money to perform completely manually. Chief among these processes is monitoring for changes to regulations, and then modifying the company’s operations to comply with them. In automating these operations, Regtech also helps a company save money that could be lost to regulatory fines for failing to follow the most current rules.

More specifically, the benefits of Regtech to companies include the following:

- Speeding up repetitive compliance tasks while reducing the risk of human error

- Smoother customer onboarding through aggregated data that avoids redundancies

- More transparent compliance programs via more accurate and frequent activity reports

- Faster adaptation of systems to changes in regulatory requirements

On the other hand, some Regtech challenges that are emerging—and will likely continue in the future—are:

- Increasing migration of transactions to online and mobile platforms

- Constantly-changing regulations to account for the resulting surge in cybercrime

- A rapidly-growing Regtech market that provides an overwhelming amount of choice

- Disruptions to regulatory oversight caused by external crises

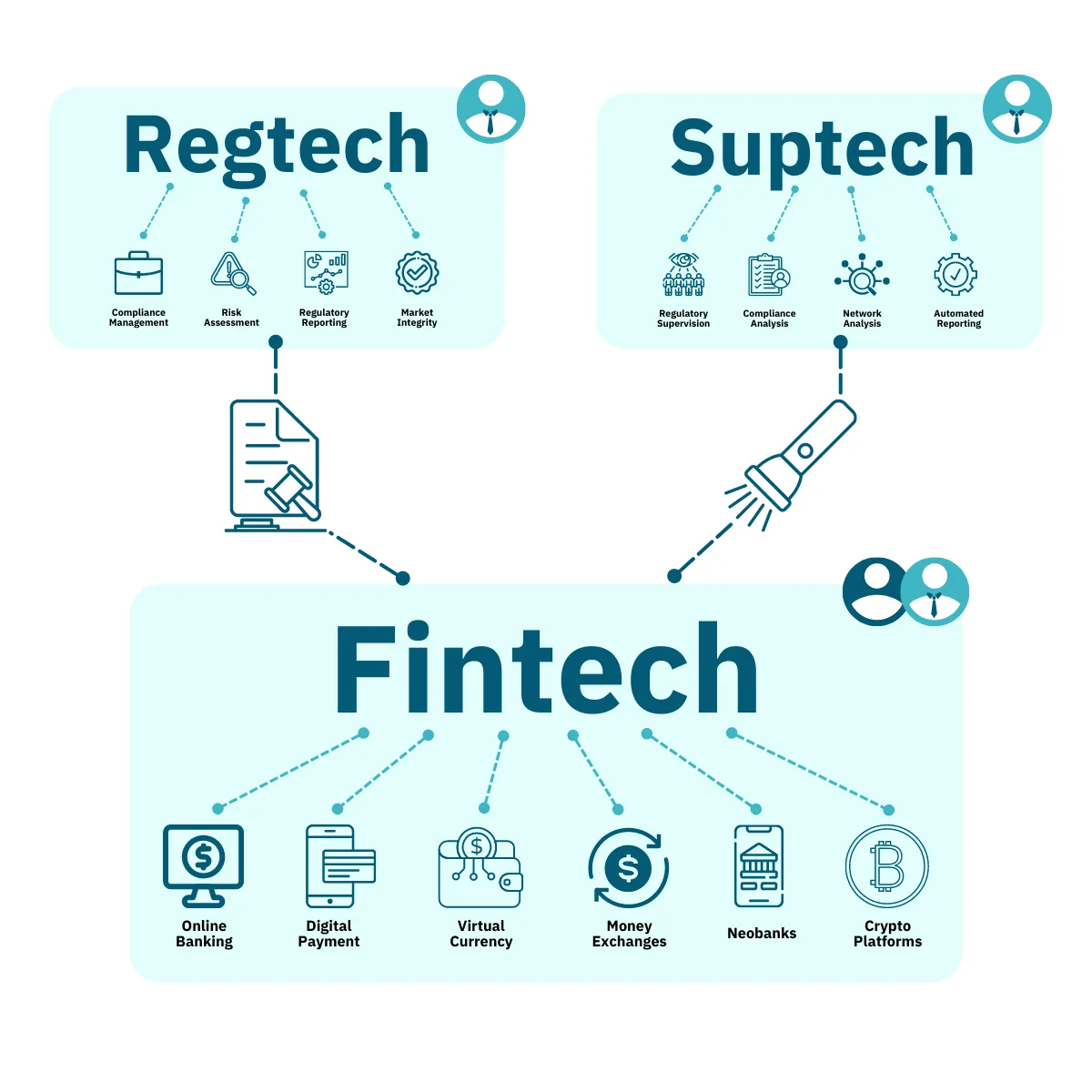

Regtech, Suptech, and Fintech Compared: The Main Differences

Regtech, Suptech, and Fintech are three terms that are often closely associated with each other. However, they each have some differences in terms of who uses them and what they are used for. We’ll expand on how they are related and what makes them unique below.

Fintech (Financial Technology)

Fintech is a broad term that refers to any technology that can help deliver or better manage financial services. It differs from Regtech and Suptech in that it’s typically seen as consumer-facing: aimed at offering accessible, convenient, and easy-to-use financial functions that traditional banks often don’t.

With that said, Fintech can also cater to financial institutions or regulatory agencies looking to streamline or even diversify their operations. This is how it relates to the other two terms.

Regtech (Regulatory Technology)

Regtech is technology aimed at helping an FI streamline regulatory compliance in its operations. Though it can be classified as a type of Fintech, it differs from most other types in that it’s meant to be business-facing instead of consumer-facing. That is, it’s there to help FIs optimize their own internal processes to be compliant with industry rules, as opposed to developing innovative new products and services to deliver to customers.

Though Suptech is also business-facing, what makes Suptech and Regtech different is the type of businesses they target. Regtech targets FIs in order for them to better manage their own compliance efforts. Suptech, meanwhile, targets regulators and auditors to help them more efficiently evaluate if FIs are following the rules correctly.

Suptech (Supervisory Technology)

Suptech is technology designed to automate, manage, and improve oversight operations. Think of it as Regtech for financial auditing and regulatory agencies: instead of helping FIs shape their operations to comply with industry rules, it helps the regulators themselves keep track of the rules and how well FIs are following them.

Suptech helps authorities take a more holistic view of the financial regulatory landscape. It looks across and between markets to identify new financial crime schemes, as well as trends in what kinds of illegalities are being committed. Then it can prioritize the issues that FIs are most vulnerable to, and develop regulations (or at least guidelines) to communicate to FIs how they can reinforce these weak points.

Regtech solutions can help a financial institution comply with industry rules aimed at preventing fraud, money laundering, and other financial crime. Here are 8 Regtech applications that make compliance-related processes faster, more effective, and less costly for financial institutions.

- Identity Verification and Management: In order to properly onboard customers and authorize their transactions, FIs need to ensure clients’ ID information corresponds to a real person (or company) and matches the person presenting it. Regtech for ID verification can analyze this information and check it automatically against multiple authoritative sources, allowing for faster and more accurate user authentication.

- Customer Due Diligence: Going a step further, Regtech can also automate checks of customers’ background information for FIs. This includes their transaction histories, business ownership status, and other finance-related behavior. Depending on the FI’s business situation and the regulations it has to comply with, Regtech for KYC can be tuned to the areas of greatest risk for fraud, money laundering, or whatever financial crimes they’re focusing on preventing.

- Transaction Monitoring and Screening: The sooner suspicious transactions are identified and acted on, the less chance they will cost an FI from being victimized by fraud or money laundering. Regtech for transaction monitoring can be used to flag and prioritize the risk levels of behavioral anomalies, based on past financial activity and current regulatory thresholds, in real time.

- Case Management and Regulatory Reporting: Cases of suspicious activity need to be reported to financial regulators promptly to avoid non-compliance penalties. Regtech can help with this by storing and visualizing relevant data for faster investigations, and auto-populating information in templates so reports get sent to authorities sooner.

- Risk Profiling and Management: Compliance teams want to avoid false positives as much as possible, and instead focus on events that have the highest likelihood of being actual fraud, money laundering, or other financial misconduct. Regtech for risk management can allow for analyzing transaction histories, background information, and other contextual indicators to predict the cases most likely to be actual threats. It can also automatically prioritize them so they get the attention they require.

- Money Laundering Detection and AML Compliance: Investigating and reporting on suspected money laundering in line with financial regulations takes a lot of time and information. Regtech for AML can make this process faster and more thorough by detecting criteria commonly associated with money laundering in events, weeding out false positives, and automatically gathering all data necessary for proper AML investigating and reporting.

- Fraud Prevention and Anti-Fraud Compliance: Fraud comes in many different forms, with fraudsters coming up with new schemes all the time. So it’s critical to have Regtech solutions that can act in real time—not only to recognize and block known fraud attempts but also to identify successful new fraud attacks so they can be properly investigated and reported on. This helps FIs limit the damage they take from fraud, avoid non-compliance penalties from financial regulators, and maintain the trust of their customers.

- Regulatory Auditing and Change Management: Financial regulations change often, usually mandating that areas not covered as comprehensively before be more strictly monitored. Regtech is critical in assessing an FI’s current compliance situation, alerting FIs to updated rules, and helping compliance teams implement necessary changes within given time limits.

Regtech is like an internal audit tool for a financial institution. Similar to how regulators and auditors use Suptech to check if an FI is complying with industry standards, FIs can use Regtech to stay a step ahead in their compliance efforts and give authorities little reason for concern.

Here are four areas in which Regtech is especially helpful towards that end.

1. Compliance Risk Management

Being non-compliant with required financial industry regulations dramatically increases an FI’s operational risk. This is partially because it opens the financial institution up to other types of risk—thefts, cyberattacks, service disruptions, illegal business practices, unethical employee conduct, and so on. Such risks can cost the FI money, digital infrastructure, employee loyalty, customer satisfaction, and even its reputation within the industry.

Regtech helps to prevent these things from happening to an FI by assisting it with compliance risk management. This involves assessing how closely the FI’s current operations align with the latest industry standards, including where they’re most vulnerable to a regulatory breach that would have serious consequences.

2. Avoiding Fines and Penalties

Besides increasing operational risks for an FI, failing to comply with industry regulations also carries the risk of being fined by supervisory authorities. For example, in March of 2023, the US Federal Reserve System and the Office of Foreign Assets Control (OFAC) fined Wells Fargo Bank $30 million and $67.8 million (respectively). Wells Fargo had provided a European bank with financial software that was used to conduct trades with entities on US sanctions lists over a period of several years.

So while compliance operations can be expensive, investing in Regtech can minimize the risk that an FI will fail to comply with regulations, resulting in even more costly fines if it’s caught. In this example, a Regtech solution could have helped Wells Fargo save nearly $100 million by realizing sooner that the people and places its software was being used to deal with were sanctioned.

3. Reporting and Case Management

According to the US Office of the Comptroller of the Currency (OCC) and Financial Crimes Enforcement Network (FinCEN), when a financial institution identifies suspicious activity, it typically has no longer than 30 days after detection to file a suspicious activity report (or 60 days if no suspect is initially found).

While these are the legal requirements, it’s generally better to file a SAR earlier so the incident gets investigated sooner and the amount of damage it does is mitigated. Regtech can help immensely with this by creating templates for properly filing reports, auto-populating them with the relevant information, and then automatically sending the report electronically to the proper authorities.

Reporting also often isn’t isn’t a one-and-done process. FIs may need to submit additional SARs no more than 120 days after the initial filing if they suspect the suspicious activity is continuing. And in any event, an FI must keep its own records of SARs for at least five years. Regtech related to case management can help keep the necessary information on SARs organized and separate, both for when an FI is audited and if further investigation on a case is required.

4. Regulatory Change Management

Financial regulations are constantly evolving in response to new technologies and shifting industry circumstances. These affect not only how people manage their finances, but also how criminals exploit systems for illegitimate gain.

Keeping up with new regulations put in place, including any deadlines an FI needs to comply with, is incredibly difficult without Regtech. This is especially true if an FI operates in multiple different jurisdictions. For example, regulatory agencies in the US may not have exactly the same rules as those in the European Union.

Regtech simplifies the process of learning about upcoming rule changes, and thus ensuring that a financial institution’s policies and procedures take these changes into account. This is important for hitting deadlines to avoid being found non-compliant.

The global Regtech market size reached $12.37 billion US in 2023, and is expected to grow to $30.4 billion US by 2027. This growth is attributed to a few things. One is the rising cost of compliance as the rates of online fraud, money laundering, and other financial crimes continue to increase. At the same time, business investors are demanding ways to perform more thorough customer due diligence on businesses to ensure they’re complying with financial regulations. And regulators themselves are looking to step up their compliance enforcement efforts, such as with the formation of the Anti-Money-Laundering Authority (AMLA) in the EU.

Other Regtech trends indicate a shift in its overall focus. Virtual currencies continue to be a hot topic for regulators, as their lack of current standards makes them ripe for fraud and money laundering. We’re also seeing more Fintech firms investing in environmental, social, and governance (ESG) applications. These may require different kinds of regulations than traditional financial use cases.

For example, “greenwashing”—making misleading claims about an organization’s environmental contributions or lack of environmental impact—has already landed even some well-established FIs in trouble with regulators. As finance and other industries increase their focus on ESG, it’s reasonable to assume that rules surrounding these practices will become stricter and more clearly-defined. Thus, Regtech will have to adapt to cover them.

There are a few predicted developments on the technical side of Regtech as well. Artificial intelligence and machine learning capabilities will likely be front and center, as financial institutions look for more efficient Regtech software to keep compliance costs down. Another emerging trend is a preference for cloud-based, software-as-a-service Regtech tools that are more accessible and offer “sandbox” staging areas with which to test threat detection.

Finally, FIs are utilizing blockchain technologies in Regtech to hinder unauthorized modification of their records. This not only helps to cut down on fraud but also increases the transparency of their compliance efforts.

Make Use of Regtech from Unit21 to Stay Afloat in the Financial Regulatory Landscape

Unit21’s Regtech infrastructure can help financial institutions keep on top of their risk and compliance obligations. Our Transaction Monitoring helps risk and compliance teams analyze not just financial deals themselves, but other related contextual data to reduce false positives and more accurately detect suspicious activity. And our Case Management solutions help speed up investigations by keeping information related to particular incidents in one spot and providing automated reporting.

See what Unit21 can do, up close and personal, by booking a demo today.