Why Device Intelligence for Fraud Detection Is No Longer Optional

Fraud teams today operate under constant pressure. Product teams want higher approval rates. Growth teams want faster onboarding. Customers expect smooth, low-friction experiences. Leadership expects fraud losses to decline, not increase.

Simply blocking more users won’t solve the problem. Approving everyone is not an option either. The most difficult fraud decisions arise when you have almost no information about the person in front of you, not after years of transaction history and clear behavioral patterns.

That is where device intelligence for fraud detection becomes essential. For fintechs and financial institutions, it serves as a foundational layer for modern fraud detection and prevention strategies.

Fraud Often Starts Before the First Transaction

Many fraud programs monitor transactions, like unusual transfers, spending anomalies, and suspicious behavior over time. But today, fraud often begins earlier, during:

- Account creation

- Login attempts

- Account takeover (ATO) attacks

- Password resets

- First-time deposits or funding

At these moments, teams face unknown users. They have no history, no established behavior, and no proven track record of trust. Yet they must decide: should they approve, step up authentication, or block?

Without strong signals at this early stage, fraud teams face a difficult trade-off: tighten controls and reduce conversions, or relax controls and accept higher losses. Neither approach works long-term.

The Ongoing Balance Between Growth and Risk

Modern fraud leaders don’t just stop bad actors. They also support growth. They reduce fraud losses without creating unnecessary friction for legitimate users. That means limiting false positives while still detecting increasingly sophisticated attacks.

When reliable signals appear only after a transaction, organizations react late. Reacting late costs money and operational efficiency. Effective fraud prevention requires confidence earlier in the customer journey. Device intelligence provides that early confidence.

Why the Device Matters So Much

When someone creates an account or logs in, their identity may still be uncertain. But one thing becomes immediately apparent: the device they are using.

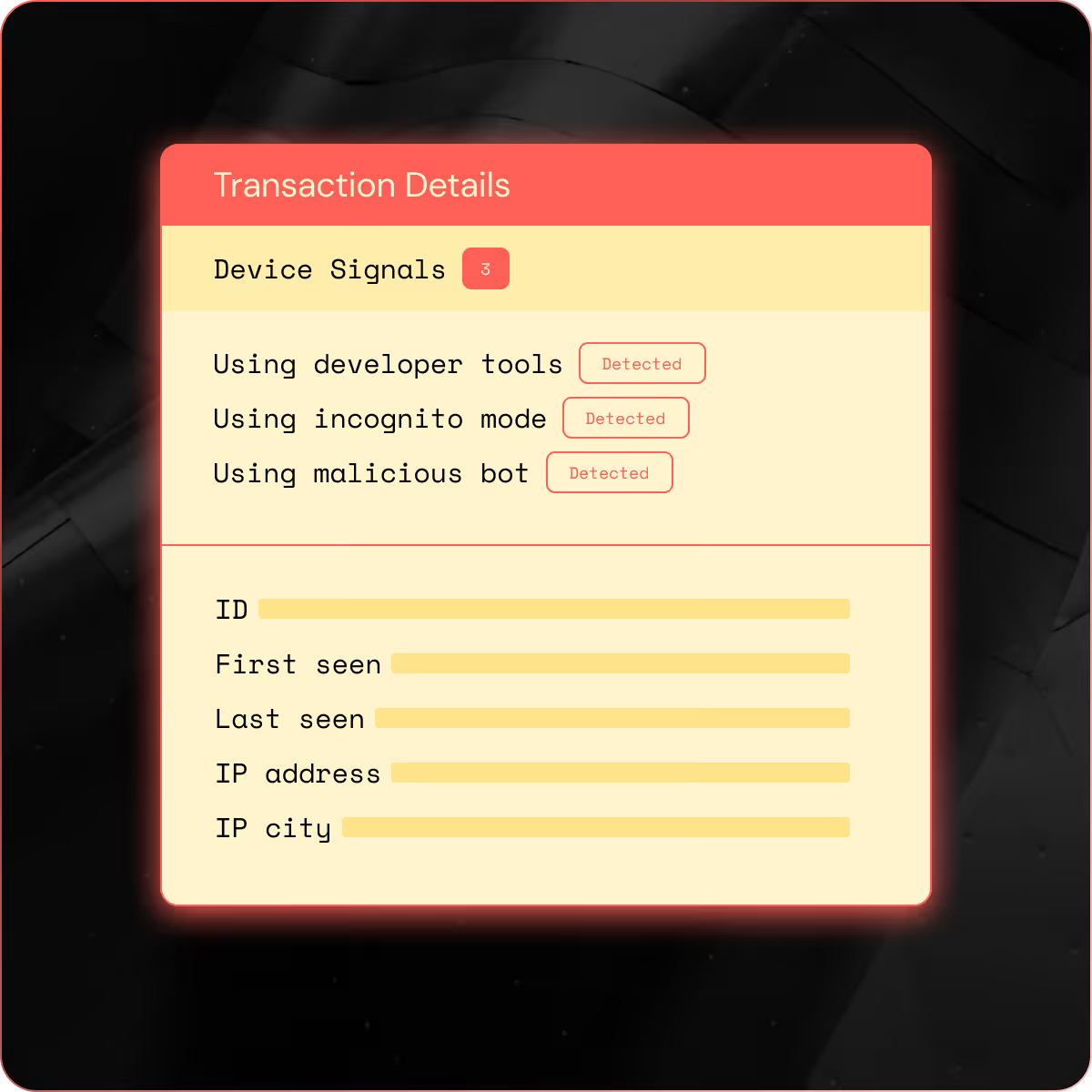

Device intelligence for fraud detection analyzes signals such as:

- Device type and operating system

- Browser and application details

- IP address and geo-location indicators

- Patterns of behavior across sessions

- Signs of VPN use, emulators, or device manipulation

These signals help answer important questions:

- Has this device been linked to fraud before?

- Does it show signs of tampering or geo-location spoofing?

- Is this login consistent with prior activity?

- Is this “new” account actually tied to an existing risk pattern?

Instead of relying only on what a user claims about themselves, teams gain objective context from their environment and behavior. For unknown users, that context can make the difference between approving with confidence and absorbing preventable losses.

While device fingerprinting focuses primarily on identifying a device, device intelligence for fraud detection goes further. It evaluates risk signals, behavioral patterns, and environmental indicators to support real-time decisions on fraud detection.

Data Alone Is Not Enough

Collecting device signals alone doesn’t solve the problem. Many organizations use standalone device-fingerprinting tools that provide raw data or a single risk score. Fraud teams then must manage separate workflows, build additional logic, or rely on opaque outputs that they struggle to explain internally or to regulators.

This approach often adds complexity rather than reducing it. Fraud teams need visibility and control. They need to:

- Use device risk scores directly within real-time rules

- Adjust thresholds without heavy engineering support

- Test new strategies before full rollout

- Combine device, behavioral, transactional, and identity data in one place

- Investigate alerts within the same system where they make decisions

When fraud teams integrate device intelligence into the broader fraud framework, it becomes far more powerful.

Fraud Is Becoming More Automated

The threat landscape keeps evolving. Fraud rings increasingly use automation and AI to create accounts at scale, distribute login attacks, and mimic legitimate behavior. Devices can be spoofed, IP addresses can rotate, and identities can be synthetic.

Volume and sophistication rise simultaneously. Fraud teams need tools that support real-time decisions, transparent risk scoring, and fast iteration. Detection and investigation must work together seamlessly.

For B2C fintechs and financial institutions in particular, where onboarding and login represent both high value and high risk, early visibility matters. The earlier teams identify risk, the less they depend on costly downstream controls and manual reviews.

A Shift in How Fraud Decisions Are Made

Fraud leaders should not view device intelligence as just another add-on capability. It changes how they approach fraud decisions. Instead of asking, “Can we catch fraud after it occurs?” they should ask, “Can we conduct a risk assessment confidently before we fully know the user?”

When teams embed device intelligence within a broader fraud detection and prevention strategy (connected to rules, real-time decisioning, investigation workflows, and AI-driven detection), it becomes more than a source of signals. It becomes a strategic advantage.

In an environment where growth and risk constantly compete, reducing uncertainty early allows organizations to protect revenue without slowing it down. Increasingly, that process begins with the device.

Strengthen Fraud Detection With Unit21’s Device Intelligence

Device intelligence for fraud teams gives the context they need to make confident decisions at the very start of the customer journey. Understanding devices, patterns, and risk signals in real time reduces uncertainty, protects revenue, and minimizes false positives.

Ready to see device intelligence in action? Unit21’s integrated device risk scoring and real-time tools can strengthen your fraud detection and prevention strategy and help your team stop fraud without slowing growth. Schedule a demo today to know more.

Gal Perelman is the Product Marketing Lead at Unit21, where she spearheads go-to-market strategies for AI-driven risk and compliance solutions. With over a decade of experience in the fintech and fraud sectors, she has led high-impact launches for products like Watchlist Screening and AI Rule Recommendations.

Previously, Gal held marketing leadership roles at Design Pickle, Sightfull, and Lusha. She holds a Master’s degree from American University and a Bachelor’s from UCLA, and is dedicated to helping banks and fintechs navigate complex regulatory landscapes through innovative technology.