Chartis names Unit21 a Category Leader in Fraud

|

Read the analyst report

Product

AI Risk Infrastructure

Detection, investigation, & decisioning in one intelligent platform

By Vertical

Fintech

Crypto

Sponsor Banks

Financial Institutions

By Persona

Fraud

AML

Integrations

Integrate with anything

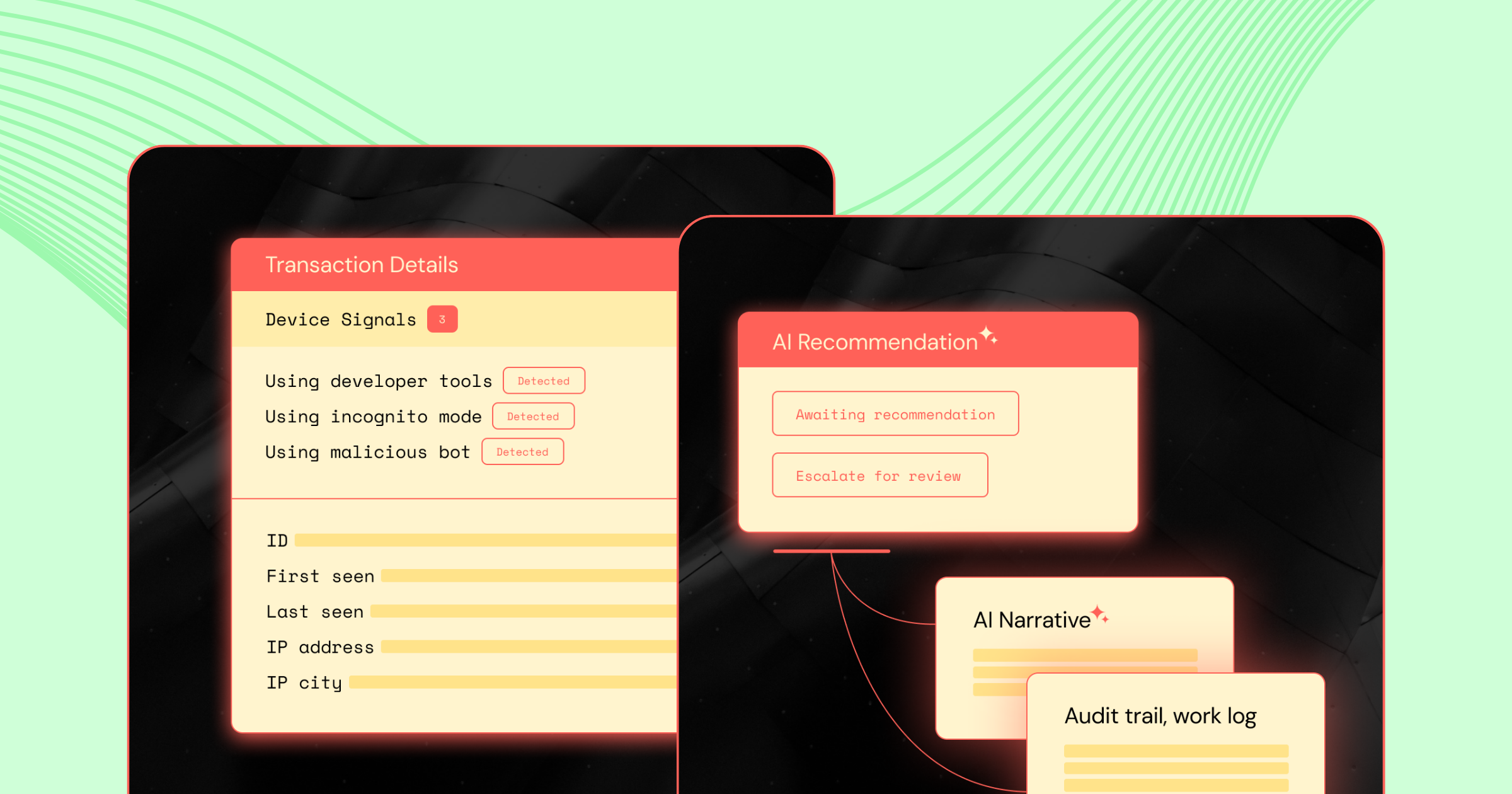

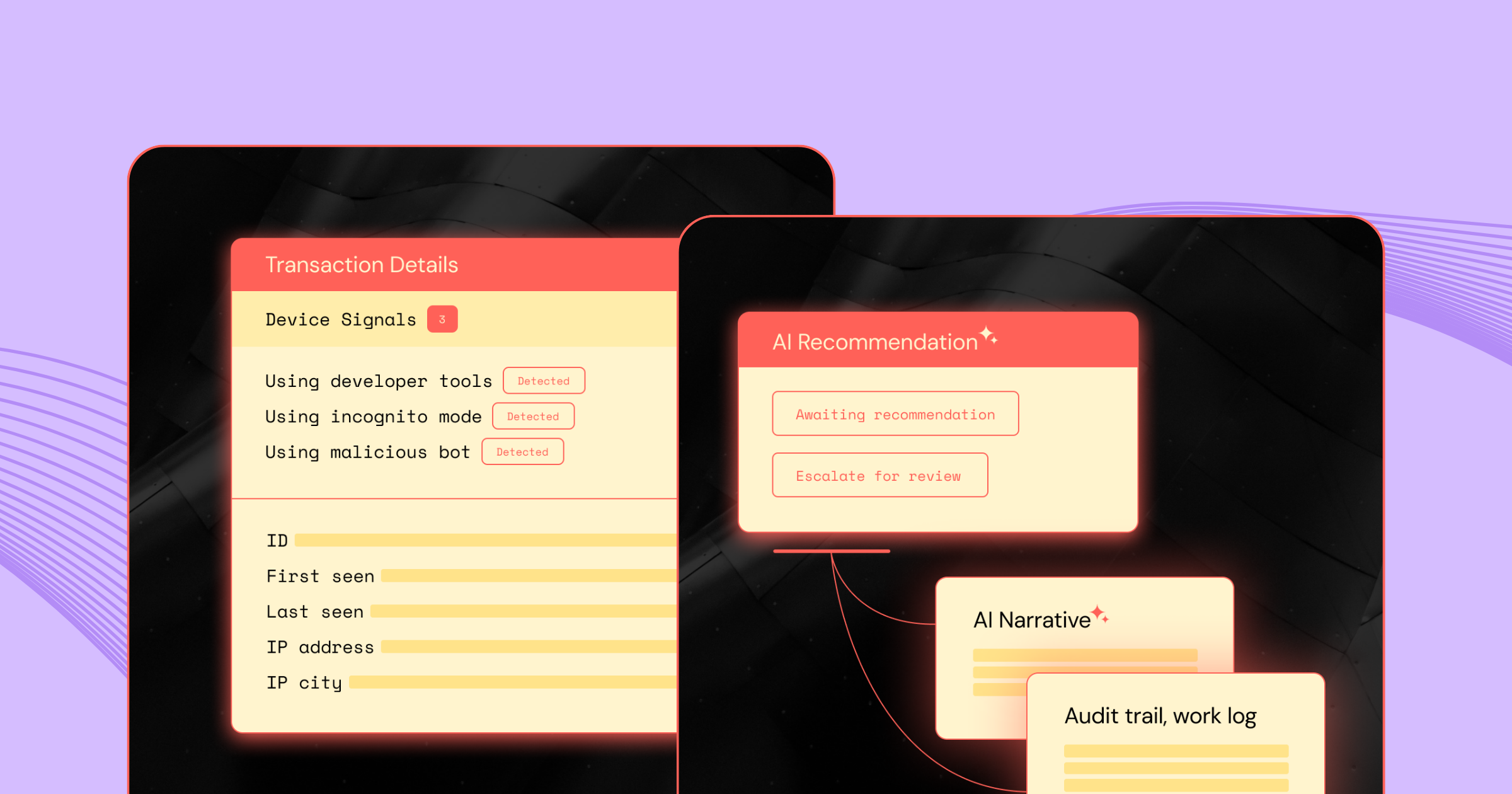

Unit21 for Fraud

Real-Time Monitoring

Device Intelligence

Consortium

Unit21 for AML

Transaction Monitoring

Case Management

Payment Screening

Sanction Screening

Customer Risk Rating

Regulatory Filings

Company

Careers

Newsroom

Contact Us

Resources

Blog

Resources

Customer Stories

Documentation

Resources for Timely Regulations

Nacha Operating Rules

FinCEN’s NPRM

Operationalizing MiCA

Analyst Research

Chartis evaluated 40+ fraud vendors. Read a deep dive on why Unit21 is a Category Leader & best in AI

Dive into findings

Customers

Get a Demo

Resources

The latest research, thought leadership, and predictions across

fraud & AML

Analyst report

Chartis evaluated 40+ fraud vendors. Read a deep dive on why Unit21 is a Category Leader & best in AI

Dive into findings

Manual

Fraud Fighters Manual

March 6, 2025

Research Report

Insights from the 3rd Annual State of Fraud and AML Report

March 6, 2025

Webinar

See it live: Building custom AI agent tasks in minutes

June 24, 2026

Webinar

The effectiveness mandate: Making sense of FinCEN's AML/CFT program NPRM

June 2, 2026

Webinar

See it live: Unit21 and FinCEN’s NPRM

May 27, 2026

Webinar

You have your MiCA license. Now what?

May 7, 2026

Webinar

Deploying the new AML playbook: Unit21 at Liminal Demo Day

April 30, 2026

Webinar

How Brex Is Building an AI-Native Compliance Program with Unit21

April 27, 2026

Webinar

NACHA 2026 in action: Unit21 does the work, live

April 20, 2026

Webinar

AI Risk Infrastructure in action: How Unit21 runs the full financial crime lifecycle

March 23, 2026

Webinar

Beyond the Prompt: Deploying Autonomous AI Agents for the 2026 Financial Crime Landscape

February 12, 2026

Webinar

The Hidden Risk in Your Partner Network: Managing Compliance Risk in Layered Fintech Relationships

February 2, 2026

Webinar

The New Risk Standard: Ownership, Agility, and the End of Black-Box Monitoring

January 23, 2026

Webinar

Designing Smarter Watchlist Screening with Built-In Intelligence

December 22, 2025

Webinar

The Hidden Layer of BaaS Every Bank Needs: Transaction Monitoring

December 15, 2025

Webinar

AI-Powered Crypto Compliance Using Integrated Intelligence

November 18, 2025

Webinar

Smarter Rules, Faster Reviews: Inside Unit21’s AI Suite

November 3, 2025

Webinar

Future-Proofing Your FinCrime Ops: Automation, AI, & Elbow Grease

October 8, 2025

Webinar

Navigating NACHA’s 2026 Operating Rules for ACH Fraud With Unit21

September 23, 2025

Webinar

How AML Teams Investigate & Report Money Laundering with Unit21

September 15, 2025

Webinar

Unit21’s Rules Engine: Mastering Real-Time Velocity Rules

September 8, 2025

Webinar

Unmasking Modern Fraud: 3 Real-World Scenarios with Fingerprint

August 8, 2025

Webinar

First-Party Fraud: From Reactive Reviews to Proactive Protection

July 28, 2025

Webinar

Supercharge Your Fraud and AML Programs with Unit21 Custom AI Agents

July 16, 2025

Webinar

How Credit Unions are Shaping the Future of Fraud & AML Strategy

July 14, 2025

Webinar

Modern Financial Crime Detection: AI & Unified Platforms in Action

June 23, 2025

Webinar

From Black Box to Blueprint: Building AI Governance & Trust in AML

June 16, 2025

Webinar

Navigating the Top Crypto Fraud and Compliance Trends in 2025

May 6, 2025

Webinar

Only Screen What Matters With Unit21’s Watchlist Solution

March 4, 2025

Webinar

The Power of Unit21’s Scams Solution Against Fraud Threats

January 30, 2025

Webinar

How Unit21’s AI Agent Automates L1 AML Reviews for Faster Results

January 23, 2025

Webinar

GenAI Impacts on Fraud & AML: The Good, Bad, and Ugly

January 7, 2025

Webinar

How to Think like a Scam Artist & Tackle the Rampant Surge Head-On

December 9, 2024

Webinar

Outsmarting Fraudsters With GenAI, Rules, & Real-Time Monitoring

November 22, 2024

Webinar

Understanding QR Scams: Trends, Cases & Customer Education

November 18, 2024

Webinar

3 Key Fraud & AML Trends Every Credit Union Should Know

October 25, 2024

Webinar

The State of Fraud & AML: 3 Key Trends Shaping Banks Today

October 9, 2024

Webinar

3 Fraud & AML Trends Influencing Fintech Strategy Today

September 6, 2024

Webinar

Don't Wait 24 Hours: How Unit21 Accelerates Fraud Response

September 3, 2024

Webinar

Strategic Approaches to Future-Proofing Fraud and Compliance

August 27, 2024

Webinar

ACH Fraud Detection Made Easy with AI and No-Code Rules

July 31, 2024

Webinar

Understanding Modern Fraud Schemes: Tactics & Prevention | Unit21

July 15, 2024

Webinar

Rule Optimization Strategies to Stay Ahead of Financial Crime

July 5, 2024

Webinar

Real-Time Monitoring: Reduce Fraud Loss with Proactive Prevention

July 5, 2024

Webinar

How to Set-Up Tailored Workflows for Operational Efficiency

July 5, 2024

Webinar

Fraud Fighters Manual: Crypto Fraud Deep Dive with Kevin Yang

July 5, 2024

Webinar

Essential Tips for Modern Fraud Risk Management and Oversight

July 5, 2024

Webinar

2024 FrAML Program: Best Practices for Fraud & AML Teams

July 5, 2024

Webinar

Unit21's AI-Powered Tools: The Future of Fraud & AML Compliance

July 5, 2024

Webinar

Real-Time ACH Fraud Defense Strategies for NACHA Compliance

July 5, 2024

Webinar

2024 BaaS Spotlight: Banks & Fintech Partnership Roundtable

July 1, 2024

Webinar

Banking on Insight: Billions of Points to Fraud Prevention

July 1, 2024

Webinar

Practical Graph-Based Rules for Real-Time Fraud Prevention

July 1, 2024

Webinar

Real-Time Risk Management for Same-Day ACH Transactions

July 1, 2024

Webinar

Protecting Against Check Fraud: Trends, Tools, and Techniques

June 5, 2024

Webinar

AI-powered Check Fraud Prevention & Investigation in Action

May 29, 2024

Content

Unit21 named Category Leader in Chartis 2026 Enterprise and Payment Fraud quadrants

May 7, 2026

Content

Fraud Monitoring Checklist

May 4, 2026

Content

Liminal Link Index Report: Friendly ACH Fraud in Banking

January 9, 2026

Content

Getting Ahead of Nacha's 2026 Changes: A Practical Guide

November 5, 2025

Content

SAR Filings Trends & How to Combat ACH Fraud Across Fintechs

August 18, 2025

Content

Redefining Risk & Compliance for Banks and Credit Unions With Unit21

July 30, 2025

Content

Unlock the Future of Risk & Compliance for Fintechs With Unit21

July 30, 2025

Content

RFP Template for AI in AML Operations

July 16, 2025

Content

AI Agents for AML Reviews

May 13, 2025

Content

The Scam-demic

March 19, 2025

Content

4 Trends for Credit Unions to Combat Fraud

December 6, 2024

Content

4 Trends for Fintech to Combat Fraud

December 3, 2024

Content

4 Trends for Banks to Combat Fraud

December 3, 2024

Content

Fraud Cannot Wait 24 Hours: What Real-Time Prevention Can Do For Your Fraud Strategy

September 24, 2024

Content

Unit21 named a Leading Vendor for AML Transaction Monitoring

July 5, 2024

Content

Risk & AML Compliance for Financial Institutions

July 5, 2024

Content

Navigating a New Frontier of Finance with Real-Time Monitoring

July 5, 2024

Content

Risk & AML Compliance for Credit Unions

July 5, 2024

Content

The Rising Tide of Check Fraud

June 11, 2024

Virtual summit

How Seraph Secure Helps Stop Scams and Protect Your Loved Ones

July 15, 2024

Virtual summit

Live AMA with Kitboga: Scams, Tactics, and Fraud Prevention Tips

July 1, 2024

Virtual summit

Proactive Fraud Prevention, Detection, & Investigation with Unit21

June 4, 2024

Virtual summit

Illicit Money Movement: Real Stories from Investigative Reporting

June 4, 2024

Virtual summit

Transform Your Financial Data Workflow with Unit21's FFIP

June 3, 2024

Virtual summit

2024 FinCrime Trends from LinkedIn’s Top Risk & Compliance Voices

June 3, 2024

Virtual summit

Pig Butchering Scams Explained: Tactics, Red Flags, & Prevention

June 3, 2024

Virtual summit

SAR Filing Automation: Simplifying FinCEN Reporting Workflows

June 3, 2024

Virtual summit

Transforming Data Into Action & AI Automation With Unit21

June 3, 2024

Virtual summit

How Banks Can Optimize a Secure and Scalable BaaS Program

May 31, 2024

Virtual summit

5 Fraud Challenges in Financial Institutions & How to Tackle Them

May 31, 2024

Virtual summit

Keanu Reeves Isn’t in Love With You: Online Romance Fraud Reality

May 31, 2024

Virtual summit

Staying Ahead of APP Fraud: Strategies for Instant Payment Safety

May 31, 2024

Virtual summit

Account Takeover Trends: Data-Driven Fraud Prevention Tips

May 30, 2024

Virtual summit

Money Laundering in Crypto & Fintech: Tactics and Prevention

May 30, 2024

Virtual summit

Live AMA: Key Trends in Check Fraud, First-Party Fraud, & AI

May 30, 2024

Virtual summit

How Collaborative Consortiums Are Strengthening Fraud Defenses

May 30, 2024

Virtual summit

Unit21’s AML Solution: Control, Visibility, and Automated Filings

May 30, 2024

Virtual summit

Quality Assurance in AML: Ensuring Accuracy and Compliance

May 30, 2024

Virtual summit

From Reactive Detection to Proactive Prevention with Unit21

May 30, 2024

Virtual summit

Unit21's ACH Risk Scores: Balancing Fraud Prevention and Speed

May 30, 2024

Virtual summit

Uncover Fraud Schemes Using Visual Connections & Graph-Based Rules

May 30, 2024

Virtual summit

AI-Powered Check Fraud Investigation & Prevention with Unit21

May 30, 2024

Virtual summit

Unit21's Fraud Consortium: Holistic Insights for Fraud Prevention

May 30, 2024

Virtual summit

Simplifying Fraud Rule Building: Tips and Tools from Unit21

May 30, 2024

Virtual summit

Fintech Spotlight: Balancing Growth with Risk in the Post-ZIRP Era

May 30, 2024

Virtual summit

Institutional Strategies for Protecting Consumers from Sextortion

May 30, 2024

Virtual summit

Inside Scambaiting: Tools and Tactics Used to Stop Online Scams

May 30, 2024

See Us In Action

Boost fraud prevention & AML compliance

Fraud can’t be guesswork. Invest in a platform that puts you back in control.

Get a Demo