AML Transaction Monitoring

Find hidden financial crime risk across your entire data ecosystem

Use all of your data, not just transactions, to uncover hidden risk. Proactively prevent financial crime, meet global regulatory expectations, and protect your organization from reputational and financial damage.

How AML transaction monitoring works

Turn data into intelligence. Automatically.

Bring in all relevant data. transactions, behaviors, devices, and customer signals, and let AI transform it into actionable risk insights.

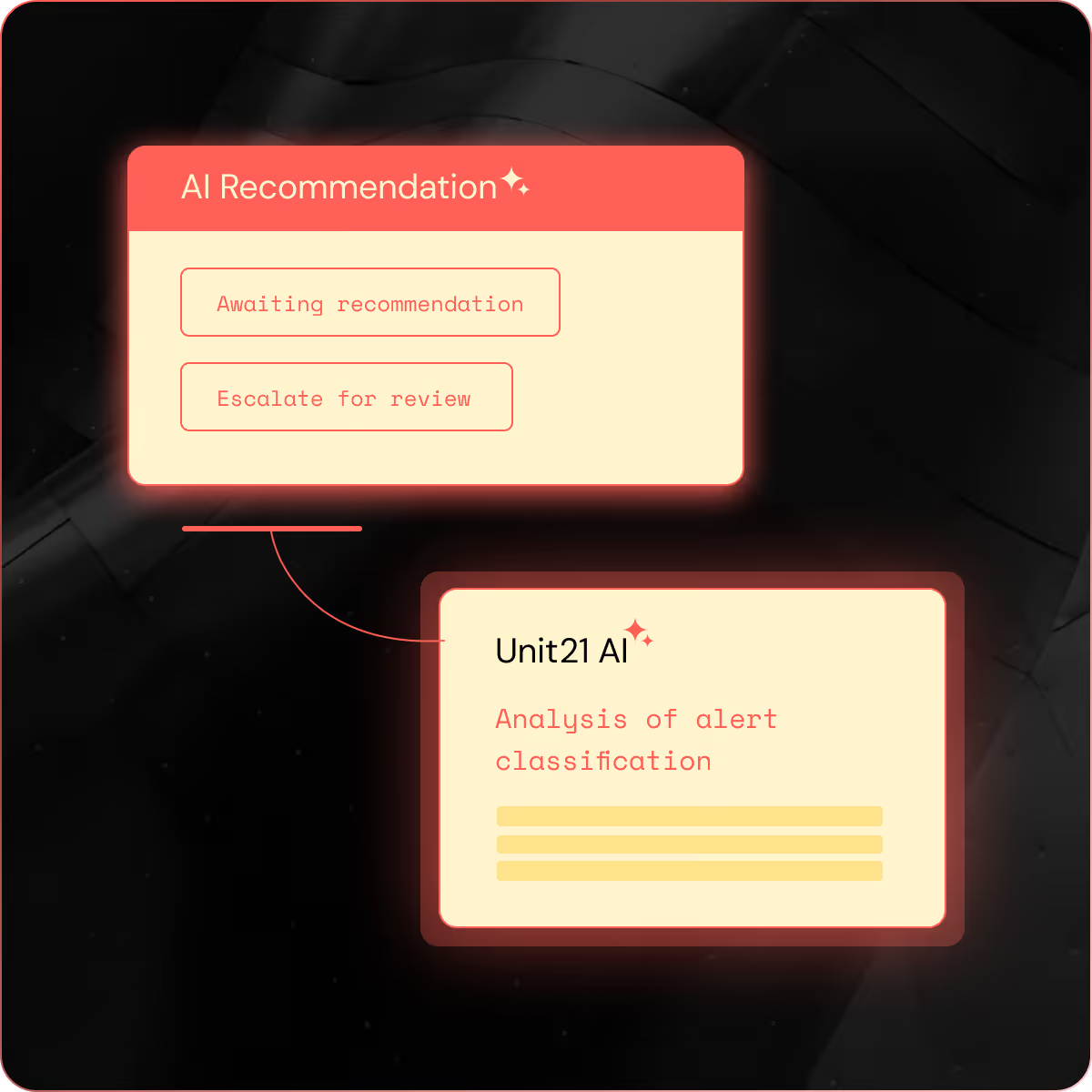

Leverage intelligent detection models alongside configurable rules, receive AI rule recommendations, validate performance with historical backtesting, and deploy with confidence, all in one unified AML platform.

What makes Unit21 transaction monitoring unique

A smarter AML platform built to adapt, not react

Traditional transaction monitoring relies on static rules and isolated data. Unit21 unifies behavioral signals, transaction data, and network intelligence, powered by AI detection and continuous rule optimization, to reduce false positives, surface hidden risk, and keep your AML program ahead of evolving threats.

Better Testing Against Any Timeframe

Reduce false positives with better test capabilities through backtesting and shadow mode against any timeframe you want. See a sample of generated alerts and iterate from there.

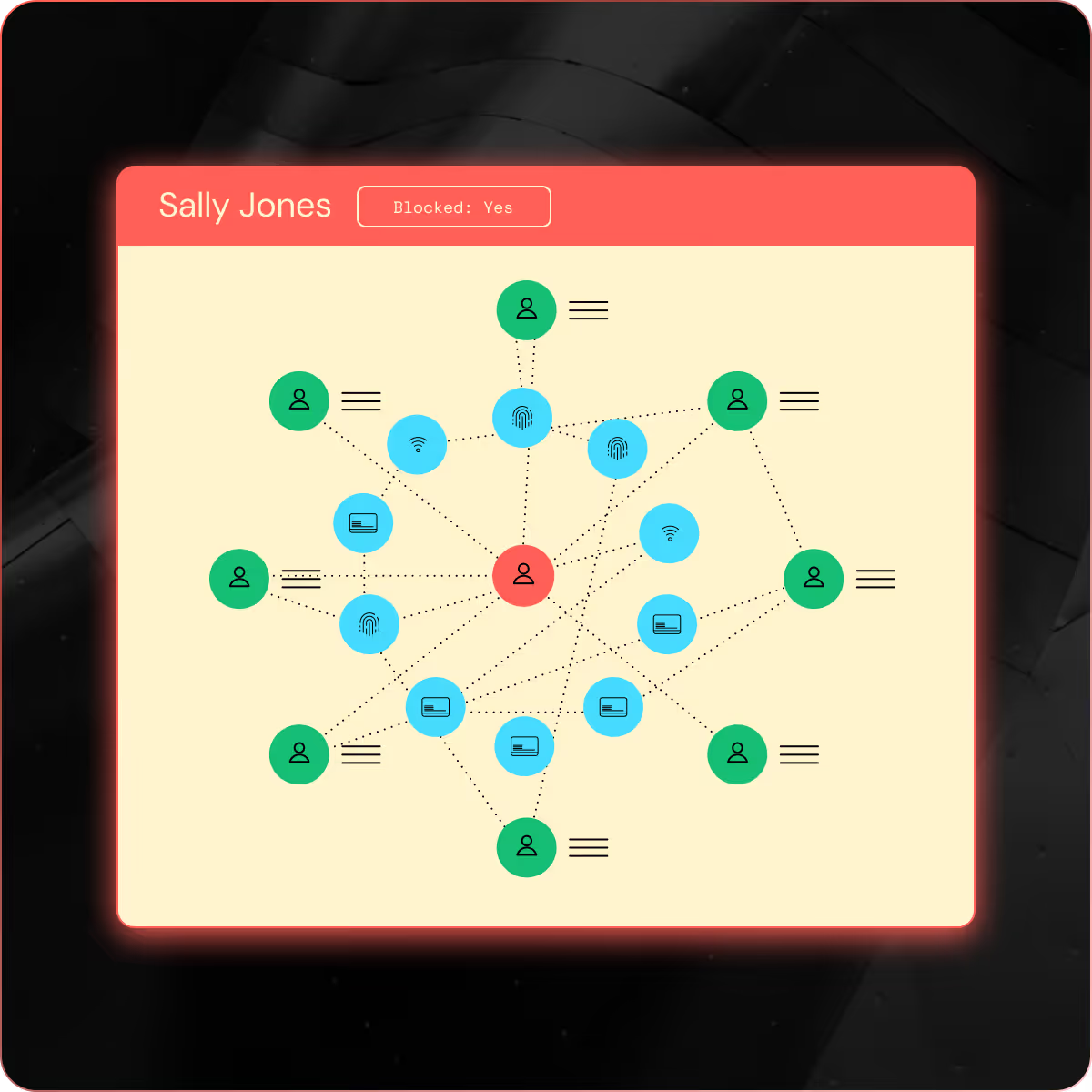

Visually Uncover Unexpected Links

With Graph-Based Rules, focus on entity relationships and patterns of shared information to uncover connections that may not be apparent with conventional methods. For example, money mules can be identified using graph-based rules, which programmatically runs link analysis across your entire dataset.

Reliable 314(a) Compliance: Every Time, with AI Precision

Our AI agent for FinCEN 314(a) quickly validates matches by comparing the key identifier, so your team focuses only on true hits. Enjoy intuitive match reviews and audit‑ready documentation, all within one streamlined platform.

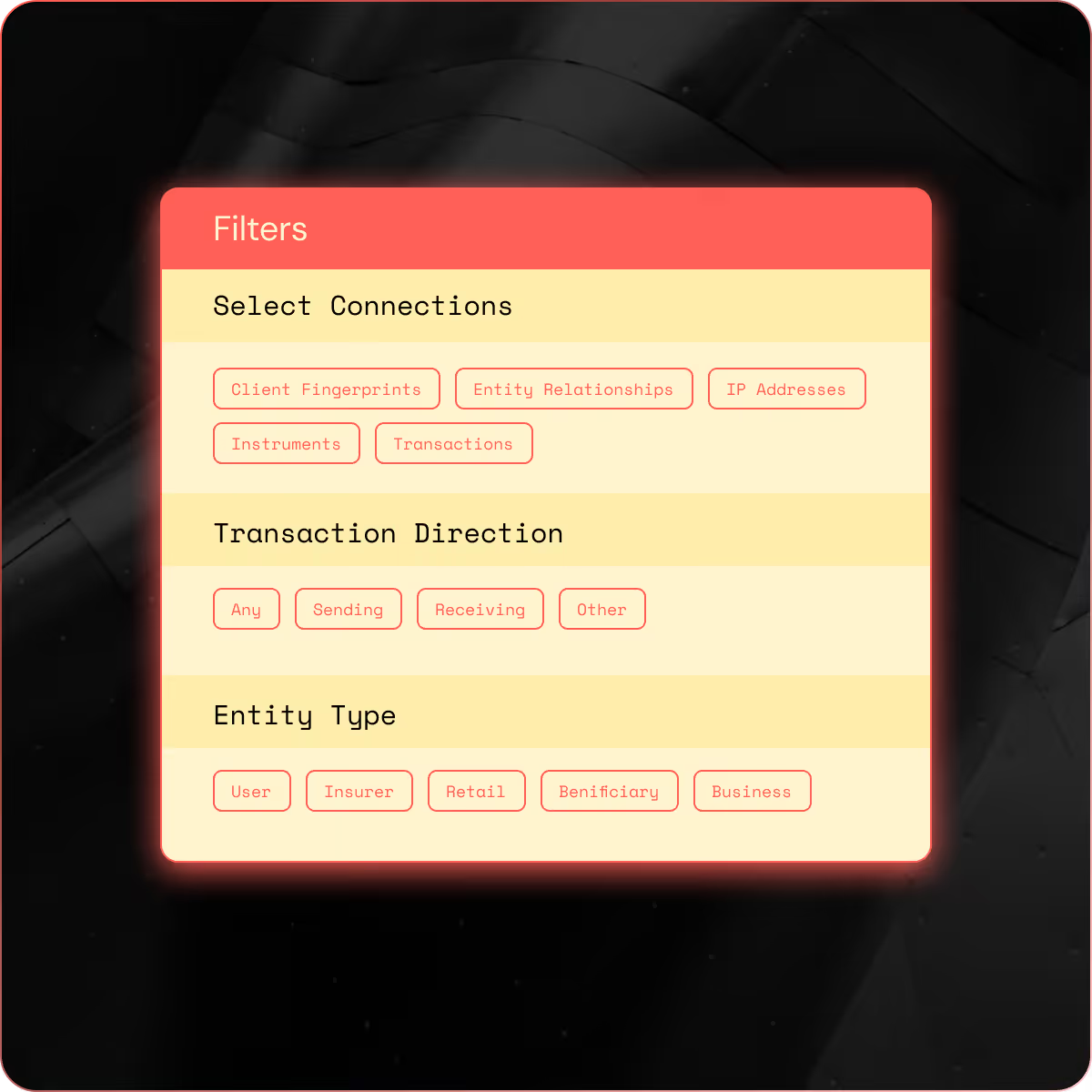

Powerful Rules & Filtering to Pinpoint Suspicious Behaviors

Use Unit21's customizable filtering to pinpoint suspicious behaviors on a particular set of transactions, accounts, devices, or customers, allowing you to run specific rules for specific types of entities, individuals, transactions, or other activities.

Your AML Program, Measured and Optimized

Monitor your AML program’s health at a glance. With 40+ dashboards, you can track alerts, cases, and SAR trends over time, measure investigator productivity, and see KPI progress across queues and dispositions. Drill down from macro program metrics to individual alerts in just a few clicks.